Vodafone Idea Share Price Target 2026, 2027, 2028, 2029, 2030, 2035, 2040, 2050: Complete Analysis and Forecast

Vodafone Idea Share Price Target

Vodafone Idea stands as India’s third-largest telecom operator, formed after the merger of Vodafone India and Idea Cellular in August 2018. The company provides mobile services, broadband, enterprise solutions, and digital platforms including Vi Movies & TV and Vi Games. Over the past seven years, the company has navigated through significant financial challenges including massive debt burdens, intense competition from Reliance Jio and Bharti Airtel, and regulatory pressures related to AGR dues.

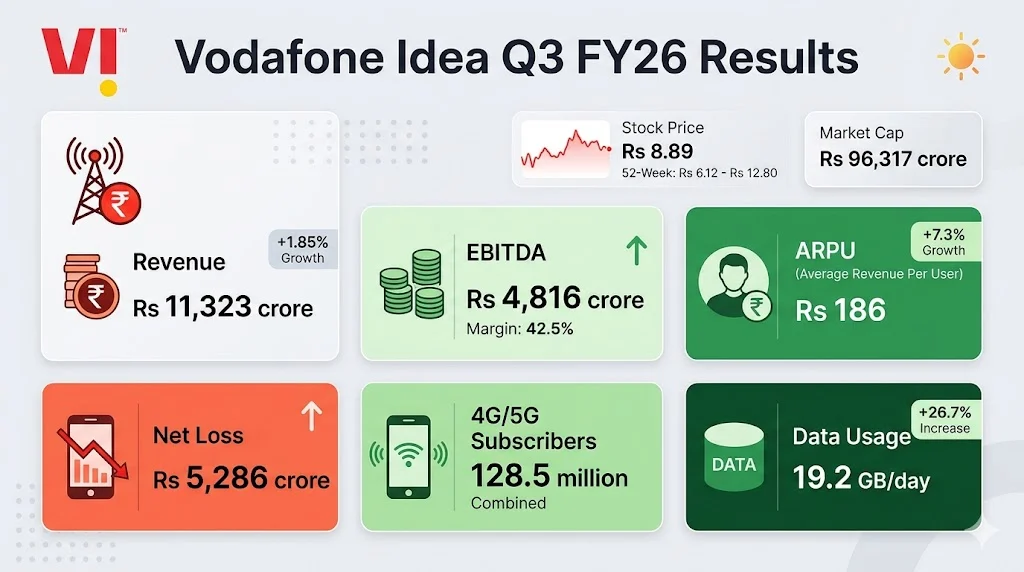

As of March 2026, Vodafone Idea trades at approximately Rs 8.89 to Rs 9.14 per share, with a market capitalization of around Rs 96,317 crore to Rs 1,00,326 crore. The stock has experienced significant volatility, trading between a 52-week low of Rs 6.12 and a 52-week high of Rs 12.80. The company continues to report net losses, but recent government relief on AGR dues and ambitious capex plans have improved investor sentiment.

In this blog post we will analysis Vodafone Idea share price target in detail from 2026 through 2050, based on fundamental analysis, technical indicators, industry trends, and expert forecasts. Investors should note that Vodafone Idea represents a high-risk, high-reward investment opportunity suitable only for those with strong risk tolerance.

Table of Contents

Vodafone Idea Current Financial Overview

Understanding the current financial position is essential before examining future price targets. The company remains in a turnaround phase with improving but still challenging metrics.

| Financial Metric | Value (Q3 FY26) | Year-Ago Comparison | Trend Assessment |

|---|---|---|---|

| Revenue from Operations | Rs 11,323 crore | Up 1.85% YoY | Modest growth |

| EBITDA | Rs 4,816 crore | Up 2.21% YoY | Stable operations |

| EBITDA Margin | 42.5% to 42.6% | +20 bps improvement | Margin expansion |

| Net Loss | Rs 5,286 crore | Down from Rs 6,609 crore | Losses narrowing |

| ARPU (Average Revenue Per User) | Rs 186 | Up 7.3% YoY | Quality improvement |

| 4G/5G Subscriber Base | 128.5 million | Up from 126.0 million | Network migration |

| Average Data Usage | 19.2 GB/day | Up 26.7% YoY | Usage growth |

| Total Debt | Rs 2,33,000 crore | High but manageable | Leverage concern |

| Cash and Cash Equivalents | Rs 3,456 crore | Limited liquidity | Funding needs |

The company reported its Q3 FY26 results in January 2026, showing a net loss of Rs 5,286 crore compared to Rs 5,524 crore in Q2 FY26, representing a 4.31% quarter-on-quarter improvement. Revenue increased 1.1% sequentially to Rs 11,323 crore, while EBITDA rose 2.8% to Rs 4,817 crore.

CEO Abhijit Kishore described the quarter as an “important inflection point” with positive resolution of key legacy issues, particularly the AGR matter. The company successfully raised Rs 3,300 crore through non-convertible debentures despite the AGR overhang, reflecting renewed lender confidence.

Key Factors Influencing Vodafone Idea Share Price

Multiple factors will determine whether Vodafone Idea achieves its price targets in the coming years. Understanding these drivers helps investors assess the probability of success.

Government Support and AGR Relief

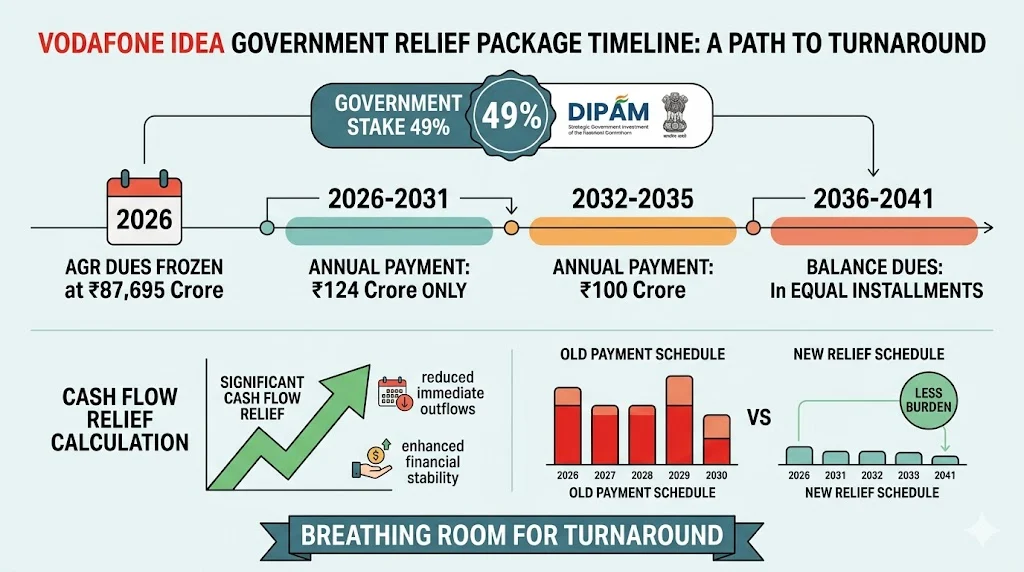

The Indian government has provided significant relief to Vodafone Idea through AGR dues restructuring. In January 2026, the Department of Telecommunications froze AGR dues at Rs 87,695 crore as of December 31, 2025, with a revised repayment framework.

Under the new schedule, Vodafone Idea will pay only Rs 124 crore annually for six years from March 2026 to March 2031, followed by Rs 100 crore annually for four years from March 2032 to March 2035. The remaining reassessed dues will be cleared in equal installments from March 2036 to March 2041 without further interest accrual.

This relief provides crucial breathing room for cash flows and removes immediate bankruptcy risk. The government currently holds approximately 49% stake in the company through equity conversion of dues, making it the largest shareholder.

Capital Expenditure Plans

Vodafone Idea has announced aggressive capex plans totaling Rs 45,000 to Rs 55,000 crore over the next three years. The company has already incurred approximately Rs 6,450 crore through nine months of FY26 and guided for Rs 7,500 to Rs 8,000 crore for the full year.

The three-year plan targets:

- Year 1: Sustained subscriber additions through network improvements

- Year 2: Achievement of double-digit revenue growth

- Year 3: Tripling of cash EBITDA

Approximately 70% of capex will fund radio access networks for 4G expansion and 5G rollout, with the remainder for transport and core infrastructure. The company plans to achieve 4G coverage parity with competitors in 17 priority circles within 12 to 24 months.

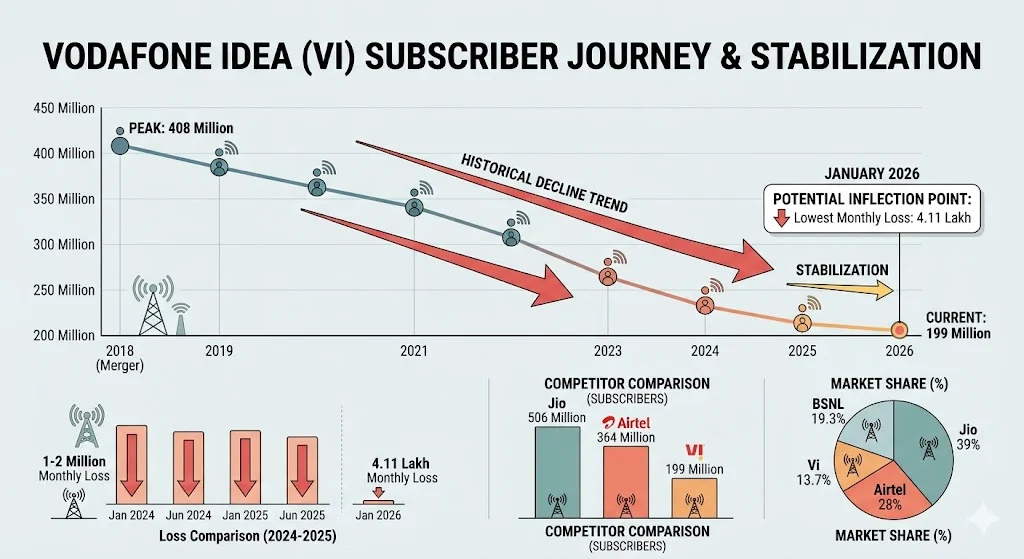

Subscriber Trends and Market Share

Vodafone Idea has experienced consistent subscriber losses since the Jio disruption, but the pace of decline has moderated significantly. The subscriber base declined from 216 million in January 2024 to approximately 199 million by December 2025.

However, January 2026 data from TRAI showed the lowest monthly loss in two years at just 4.11 lakh subscribers, compared to sustained losses of 1 to 2 million monthly through most of 2024 and 2025. This stabilization represents a potential inflection point.

The company’s market share has declined to approximately 13.7%, near all-time lows according to Jefferies analysis. Jio and Airtel continue gaining share, with the market effectively becoming a duopoly at the top.

ARPU Improvement Strategy

Average Revenue Per User remains a critical metric for telecom profitability. Vodafone Idea’s ARPU of Rs 186 trails competitors significantly:

- Bharti Airtel: Rs 259 (Q3 FY26)

- Reliance Jio: Rs 213.7 (Q3 FY26)

- Vodafone Idea: Rs 186 (Q3 FY26)

The company is implementing several strategies to improve ARPU:

- Focus on premium subscribers and quality upgrades

- Discontinuation of low-value entry-level plans

- Tariff hikes implemented in July 2024

- Potential additional tariff hikes in H1 FY27

- Migration of 2G users to 4G/5G networks

Analysts expect another round of telecom tariff hikes in the first half of FY27, which could significantly boost ARPU across the sector.

Competition and Industry Structure

The Indian telecom market has effectively become a duopoly, with Jio and Airtel controlling approximately 75% market share. Vodafone Idea faces intense competition from these well-capitalized rivals.

Jio continues aggressive expansion with 506.4 million subscribers as of Q2 FY26, adding 8.3 million users in the quarter. Airtel maintains premium positioning with 364.2 million subscribers and industry-leading ARPU of Rs 256.

Vodafone Idea’s challenge is to differentiate through service quality improvements while competing on price. The company’s partnership with AST SpaceMobile for satellite-based direct-to-device connectivity represents one potential differentiator.

Also Read: Powerful Stock Market Portfolio Strategies: Smart Investor’s Blueprint In 2026

Vodafone Idea Share Price Target 2026

The year 2026 represents a base-building phase for Vodafone Idea as it implements its turnaround strategy. The stock will likely remain volatile, reacting to news flow on fundraising, subscriber trends, and quarterly results.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 22 | Rs 26 | Q3 FY26 results, AGR relief implementation |

| February | Rs 23 | Rs 27 | Subscriber data, tariff hike speculation |

| March | Rs 22 | Rs 26 | FY26 close, annual results preview |

| April | Rs 21 | Rs 25 | Q4 FY26 results, FY27 guidance |

| May | Rs 22 | Rs 26 | 5G expansion updates, capex progress |

| June | Rs 23 | Rs 27 | Monsoon season impact, data usage trends |

| July | Rs 24 | Rs 28 | Potential tariff hike implementation |

| August | Rs 23 | Rs 27 | Q1 FY27 results, ARPU improvement |

| September | Rs 24 | Rs 28 | Festive season demand, network upgrades |

| October | Rs 23 | Rs 27 | Q2 FY27 results, subscriber trends |

| November | Rs 24 | Rs 28 | Annual planning, FY28 outlook |

| December | Rs 24 | Rs 28 | Year-end positioning, 2027 target revisions |

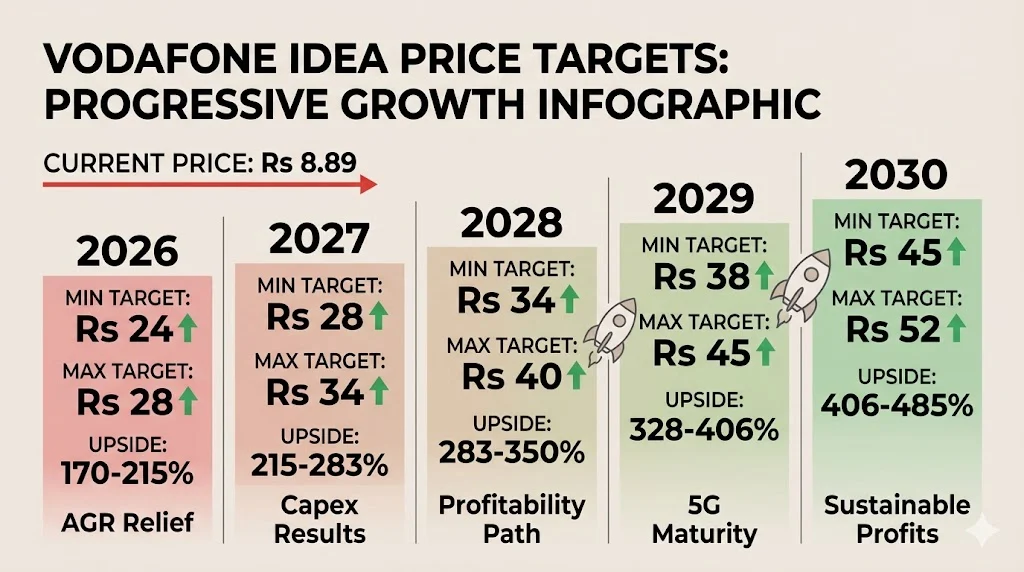

2026 Year-End Target: Rs 24 to Rs 28

The 2026 price target range of Rs 24 to Rs 28 represents a potential upside of 160% to 205% from current levels. This target assumes successful execution of the capex plan, stabilization of subscriber losses, and ARPU improvement to Rs 200+.

Key risks to the 2026 target include:

- Delay in tariff hikes due to competitive pressure

- Continued subscriber losses exceeding projections

- Inability to complete planned fundraising

- Network quality improvements falling short of expectations

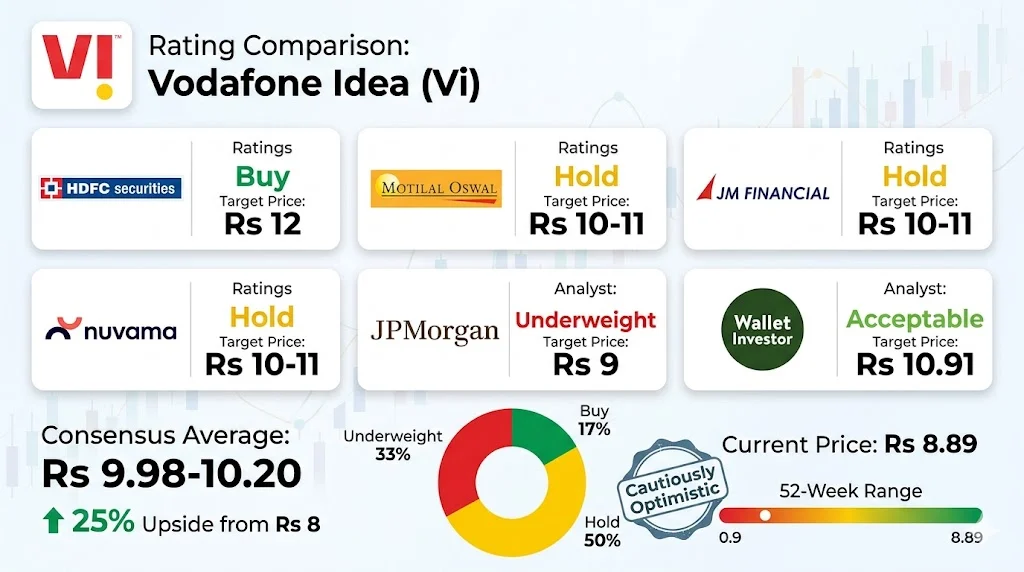

HDFC Securities maintains a Buy rating with a target of Rs 12, representing 25% upside from recent levels of Rs 8.50 to Rs 9.50. This more conservative target reflects execution risks and competitive challenges.

Vodafone Idea Share Price Target 2027

By 2027, Vodafone Idea should begin showing tangible results from its three-year capex program. The company targets double-digit revenue growth and significant EBITDA improvement by the third year of its plan.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 26 | Rs 30 | FY27 guidance, annual results |

| February | Rs 27 | Rs 31 | Full-year FY26 results, auditor comments |

| March | Rs 26 | Rs 30 | Q4 FY27 close, FY28 planning |

| April | Rs 27 | Rs 32 | Q1 FY28 results, summer season demand |

| May | Rs 28 | Rs 33 | 5G coverage expansion, city additions |

| June | Rs 27 | Rs 32 | Monsoon impact, rural network performance |

| July | Rs 28 | Rs 34 | Second anniversary of tariff hikes |

| August | Rs 29 | Rs 35 | Q2 FY28 results, ARPU trajectory |

| September | Rs 30 | Rs 36 | Festive season, data consumption surge |

| October | Rs 29 | Rs 35 | Q3 FY28 results, half-year review |

| November | Rs 30 | Rs 36 | Annual guidance, investor presentations |

| December | Rs 28 | Rs 34 | Year-end consolidation, 2028 outlook |

2027 Year-End Target: Rs 28 to Rs 34

The 2027 target range reflects expectations of operational stabilization. By this point:

- 4G coverage should reach parity with competitors in priority circles

- 5G services should be available in all major cities

- ARPU should approach Rs 220 to Rs 240

- Subscriber losses should have stopped or reversed

- Cash EBITDA should show meaningful improvement

The company aims to triple cash EBITDA by the third year of its capex plan, which would significantly improve investor confidence and valuation multiples.

Vodafone Idea Share Price Target 2028

By 2028, Vodafone Idea could approach operational breakeven if execution remains on track. The benefits of network investments should become visible in subscriber retention and ARPU growth.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 30 | Rs 36 | FY28 annual results, three-year review |

| February | Rs 31 | Rs 37 | Full-year FY28 results, profitability timeline |

| March | Rs 30 | Rs 36 | Q4 FY28 close, FY29 guidance |

| April | Rs 31 | Rs 38 | Q1 FY29 results, summer demand |

| May | Rs 32 | Rs 39 | 5G monetization, enterprise services |

| June | Rs 31 | Rs 38 | Monsoon season, network resilience |

| July | Rs 32 | Rs 40 | Potential tariff adjustments |

| August | Rs 33 | Rs 41 | Q2 FY29 results, ARPU comparison |

| September | Rs 34 | Rs 42 | Festive demand, digital services growth |

| October | Rs 33 | Rs 41 | Q3 FY29 results, half-year performance |

| November | Rs 34 | Rs 42 | Annual planning, long-term strategy |

| December | Rs 34 | Rs 40 | Year-end targets, 2029 outlook |

2028 Year-End Target: Rs 34 to Rs 40

The 2028 target assumes Vodafone Idea achieves:

- Sustainable subscriber base of 200+ million

- ARPU of Rs 240 to Rs 260, approaching Airtel levels

- Revenue growth of 12% to 15% annually

- EBITDA margins above 45%

- Path to net profitability visible within 2 to 3 years

Network quality improvements should reduce churn and support premium pricing. Enterprise solutions and digital platforms may contribute new revenue streams.

Vodafone Idea Share Price Target 2029

By 2029, the telecom industry will be fully transformed by 5G technology and digital services. Vodafone Idea’s success will depend on capturing its share of this growth.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 35 | Rs 42 | FY29 annual results, five-year review |

| February | Rs 36 | Rs 43 | Full-year FY29 results, profitability status |

| March | Rs 35 | Rs 42 | Q4 FY29 close, FY30 guidance |

| April | Rs 36 | Rs 44 | Q1 FY30 results, network performance |

| May | Rs 37 | Rs 45 | 5G services maturity, IoT revenue |

| June | Rs 36 | Rs 44 | Monsoon impact, infrastructure resilience |

| July | Rs 37 | Rs 46 | Tariff optimization, premium plans |

| August | Rs 38 | Rs 47 | Q2 FY30 results, ARPU leadership |

| September | Rs 38 | Rs 45 | Festive season, data monetization |

| October | Rs 37 | Rs 44 | Q3 FY30 results, strategic review |

| November | Rs 38 | Rs 45 | Annual guidance, dividend speculation |

| December | Rs 38 | Rs 45 | Year-end positioning, 2030 outlook |

2029 Year-End Target: Rs 38 to Rs 45

By 2029, Vodafone Idea should be approaching sustainable profitability if turnaround efforts succeed. Key milestones include:

- Net profitability achieved or imminent

- Debt reduction program underway

- Potential for modest dividend initiation

- Market share stabilization above 15%

- ARPU of Rs 260 to Rs 280

The company should benefit from industry-wide tariff increases and data consumption growth. Enterprise services, IoT, and digital platforms should contribute meaningfully to revenue.

Vodafone Idea Share Price Target 2030

By 2030, Vodafone Idea aims to be a fully transformed telecom operator with sustainable profitability and growth momentum.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 40 | Rs 48 | FY30 annual results, decade review |

| February | Rs 41 | Rs 49 | Full-year FY30 results, dividend policy |

| March | Rs 40 | Rs 48 | Q4 FY30 close, FY31 guidance |

| April | Rs 41 | Rs 50 | Q1 FY31 results, growth trajectory |

| May | Rs 42 | Rs 51 | 5G Advanced, next-gen services |

| June | Rs 41 | Rs 50 | Monsoon performance, rural expansion |

| July | Rs 42 | Rs 52 | Tariff leadership, premium positioning |

| August | Rs 43 | Rs 53 | Q2 FY31 results, market share gains |

| September | Rs 44 | Rs 54 | Festive season, record data usage |

| October | Rs 43 | Rs 52 | Q3 FY31 results, strategic milestones |

| November | Rs 44 | Rs 53 | Annual planning, 2035 vision |

| December | Rs 45 | Rs 52 | Year-end targets, long-term outlook |

2030 Year-End Target: Rs 45 to Rs 52

The 2030 target range represents a potential 400% to 470% return from current levels over five years. This assumes:

- Consistent profitability achieved

- Revenue of Rs 60,000+ crore

- EBITDA margins of 45% to 48%

- Net profit of Rs 5,000+ crore

- Debt-to-EBITDA below 3x

- Regular dividend payments initiated

- Market share stabilized at 15% to 18%

By 2030, the Indian telecom market should exceed $45 billion in annual revenues according to Jefferies estimates, with Vodafone Idea capturing its proportionate share.

Vodafone Idea Share Price Target 2035

Looking further ahead to 2035, Vodafone Idea’s success will depend on maintaining competitiveness in a rapidly evolving telecom landscape.

| Scenario | Minimum Price Target | Maximum Price Target | Probability Assessment |

|---|---|---|---|

| Bull Case | Rs 60 | Rs 75 | 30% probability |

| Base Case | Rs 45 | Rs 55 | 50% probability |

| Bear Case | Rs 25 | Rs 35 | 20% probability |

2035 Target: Rs 45 to Rs 75

By 2035, the telecom sector will be driven by:

- 6G technology development and early deployment

- Massive IoT connectivity

- Digital economy integration

- Satellite-based services

- AI-powered network optimization

Vodafone Idea’s ability to invest in these technologies while maintaining profitability will determine its long-term position. The company must avoid falling further behind Jio and Airtel in technology leadership.

Vodafone Idea Share Price Target 2040

By 2040, Vodafone Idea could be a mature telecom player if it successfully navigates the challenges of the 2020s and 2030s.

| Scenario | Minimum Price Target | Maximum Price Target | Key Drivers |

|---|---|---|---|

| Bull Case | Rs 80 | Rs 100 | Market leadership, innovation |

| Base Case | Rs 55 | Rs 70 | Stable operations, steady growth |

| Bear Case | Rs 30 | Rs 45 | Continued marginalization |

2040 Target: Rs 55 to Rs 100

The 2040 target range reflects significant uncertainty over such long time horizons. Key variables include:

- Evolution of telecom technology beyond 5G/6G

- Regulatory environment and spectrum policy

- Competitive dynamics with potential new entrants

- Vodafone Idea’s ability to maintain technology parity

- Capital allocation discipline and shareholder returns

Vodafone Idea Share Price Target 2050

Projecting to 2050 involves substantial speculation, but provides a framework for long-term thinking.

| Scenario | Minimum Price Target | Maximum Price Target | Long-Term Vision |

|---|---|---|---|

| Bull Case | Rs 120 | Rs 180 | Industry leader, global expansion |

| Base Case | Rs 80 | Rs 120 | Stable Indian operator, solid returns |

| Bear Case | Rs 40 | Rs 60 | Marginal player, limited growth |

2050 Target: Rs 80 to Rs 180

By 2050, Vodafone Idea could be a completely transformed entity, potentially:

- Integrated digital services provider beyond traditional telecom

- Leader in next-generation connectivity (quantum, satellite, etc.)

- Significant enterprise and government services provider

- Potential for international expansion or strategic partnerships

- Mature dividend-paying stock with stable returns

Investment Analysis: Bull Case vs Bear Case

Bull Case Arguments

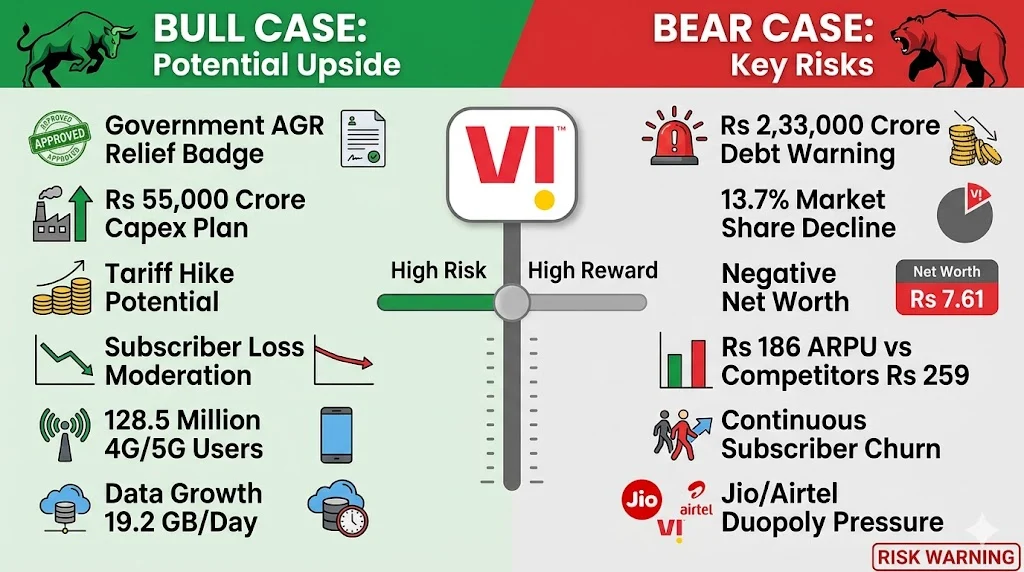

- Government support through AGR relief provides crucial breathing room for cash flows

- Large capex plan of Rs 45,000 to 55,000 crore demonstrates commitment to network improvement

- Potential tariff hikes in FY27 could significantly boost ARPU and profitability

- Data consumption growth in India remains strong with increasing smartphone penetration

- Successful fundraising and lender confidence shown through Rs 3,300 crore NCD issuance

- Subscriber losses moderating significantly with potential inflection point reached

- 4G/5G subscriber base growing with higher ARPU customers

- Enterprise services and digital platforms offer new revenue opportunities

- Duopoly structure at top provides pricing power to remaining players

- Potential for strategic investor entry at attractive valuations

Bear Case Arguments

- Continuous subscriber losses despite moderation, with base down to 193 to 205 million

- High debt burden of Rs 2,33,000 crore remains a significant overhang

- Negative net worth and negative book value of Rs 7.61 per share

- Intense competition from Jio and Airtel with much stronger balance sheets

- Network quality issues persist with frequent call drops and slow speeds

- ARPU significantly trails competitors (Rs 186 vs Rs 259 for Airtel)

- Market share at all-time lows of approximately 13.7%

- Execution risk on ambitious capex plans given historical underperformance

- Dependence on government support raises regulatory risk

- Potential for further equity dilution through fundraising

- Jio IPO expected in FY27 could intensify competitive pressure

Shareholding Pattern and Institutional Interest

Understanding who owns Vodafone Idea provides insight into market confidence levels.

| Shareholder Category | Holding Percentage | Trend | Implication |

|---|---|---|---|

| Promoters (Aditya Birla + Vodafone Group) | 25.57% | Declining from 49.6% in FY21 | Dilution through fundraising |

| Government (DIPAM) | 49.00% | Increased through equity conversion | Largest shareholder, strategic interest |

| Foreign Institutional Investors (FIIs) | 5.99% to 6.00% | Low relative to peers | Limited foreign confidence |

| Mutual Funds | 4.55% | Moderate | Some domestic institutional interest |

| Insurance Companies | 0.15% | Very low | Risk-averse investors staying away |

| Retail and Other Investors | 62.83% to 13.83% | High retail interest | Speculative retail participation |

The high retail shareholding of over 60% indicates significant speculative interest rather than institutional confidence. Promoter holding has declined steadily from 49.6% in FY21 to 25.57% currently, reflecting dilution through multiple fundraising rounds.

The government’s 49% stake provides stability but also raises questions about eventual exit strategy and impact on share price when that occurs.

Analyst Ratings and Consensus Targets

Brokerage houses maintain mixed views on Vodafone Idea, reflecting the high-risk nature of the investment.

| Brokerage | Rating | Target Price | Key Thesis |

|---|---|---|---|

| HDFC Securities | Buy | Rs 12 | AGR relief positive, add on dips Rs 8-9 |

| Motilal Oswal | Hold/Neutral | Rs 10-11 | Execution risks remain |

| JM Financial | Hold | Rs 10-11 | Ambitious plans, delayed tariff hikes |

| Nuvama | Hold | Rs 10-11 | Revised down from Rs 12 |

| JPMorgan | Underweight | Rs 9 | 23% downside risk, technical deterioration |

| Consensus Average | Hold | Rs 9.98-10.20 | 25% upside from Rs 8 levels |

| Wallet Investor (AI) | Acceptable long-term | Rs 10.91 by 2031 | +19% over 5 years |

The consensus view is cautiously optimistic with significant caveats. Most analysts acknowledge the AGR relief as a major positive but remain concerned about execution risks and competitive positioning.

Key Monitorables for Investors

Investors considering Vodafone Idea should track these metrics closely:

Quarterly Results

- Revenue growth rate (targeting double-digit by FY28)

- EBITDA margin expansion (currently 42.5%)

- Net loss trajectory (narrowed to Rs 5,286 crore in Q3 FY26)

- ARPU improvement (Rs 186 currently, targeting Rs 220+)

- Subscriber base trends (watch for inflection to growth)

Operational Metrics

- 4G/5G subscriber additions

- Data usage per subscriber (19.2 GB/day currently)

- Network quality improvements (call drops, data speeds)

- Churn rate reduction

- Market share stabilization

Financial Health

- Debt reduction progress

- Cash flow generation

- Fundraising completion

- Interest coverage improvement

- Path to profitability timeline

Industry Dynamics

- Tariff hike implementation and acceptance

- Competitive intensity from Jio and Airtel

- Regulatory developments

- Spectrum auction participation

- Technology evolution (5G Advanced, 6G)

Conclusion: Is Vodafone Idea a Good Investment?

Vodafone Idea represents one of the highest-risk, highest-potential-reward investments in the Indian stock market. The company is attempting a turnaround against significant odds, but recent government support and management commitment provide a foundation for potential success.

Suitable for:

- High-risk investors with strong risk tolerance

- Those believing in the turnaround story and management execution

- Investors seeking multi-bagger potential over 5 to 10 years

- Those comfortable with high volatility and potential significant losses

Not suitable for:

- Conservative investors seeking stable returns

- Those needing dividend income (currently zero)

- Investors uncomfortable with high debt and negative net worth

- Those requiring liquidity or short-term returns

- Risk-averse portfolios

The share price targets presented in this analysis range from Rs 24-28 for 2026 to Rs 45-52 for 2030, with long-term targets of Rs 55-100 by 2040. These represent potential returns of 160% to 470% from current levels over 5 years, but come with substantial risk of capital loss if the turnaround fails.

Investors should allocate only a small portion of their portfolio to this speculative position, diversify across other telecom or infrastructure plays, and maintain realistic expectations about execution timelines. The coming 12 to 18 months will be critical in determining whether Vodafone Idea can successfully transform from a struggling operator to a viable competitor in India’s telecom duopoly.

Always conduct thorough due diligence, consult with financial advisors, and invest only what you can afford to lose. Past performance and price targets are not guarantees of future results.

Related Posts :

Share This Post