Government Loan Schemes In India 2026: 10 Powerful Options To Start Business [With Calculators]

Government Loan Schemes In India 2026 | Image Via © thenewsminute.com

Starting a business in India is exciting, but let’s be real, funding is where most people get stuck. That’s exactly where government loan schemes in India step in. If you’ve been searching for options like Mudra loan, MSME loans, or startup funding, this guide will actually clear things up in a practical way.

Most articles just list schemes and move on. But as someone trying to apply, you need clarity on eligibility, real benefits, and what actually works on the ground. Based on updated 2026 insights and real user sentiment, this article breaks everything down in a way that actually helps you take action.

In this blog post we are going to see the Government Loan Schemes that you should know if you want to start a business. I have also included the emi calculators of each gov scheme to make this post more interactive.

Table of Contents

Key Takeaways

- Government loan schemes offer collateral-free funding for small businesses and startups

- Top schemes include Mudra, PMEGP, CGTMSE, Stand-Up India, and PM Vishwakarma

- Women, SC/ST entrepreneurs, and MSMEs get priority benefits

- Digital application and faster approvals are trending in 2026

- Repayment discipline helps unlock higher loan limits

- Real success stories show people scaling from small setups to full businesses

Why Government Loan Schemes Matter In 2026

Let’s keep it simple. Banks don’t easily give loans without collateral. That’s why these schemes exist. The government is pushing Atmanirbhar Bharat, job creation, and MSME growth. These schemes are designed to:

- Help first-time entrepreneurs

- Support small businesses with low capital

- Boost rural and women-led businesses

- Reduce dependency on private lenders

And honestly, this is working. Many small vendors, tailors, and even home-based businesses have scaled into proper companies using these loans.

Top 10 Government Loan Schemes You Should Know

Here’s a clear breakdown of the most useful schemes in 2026. Not just names, but what they actually offer.

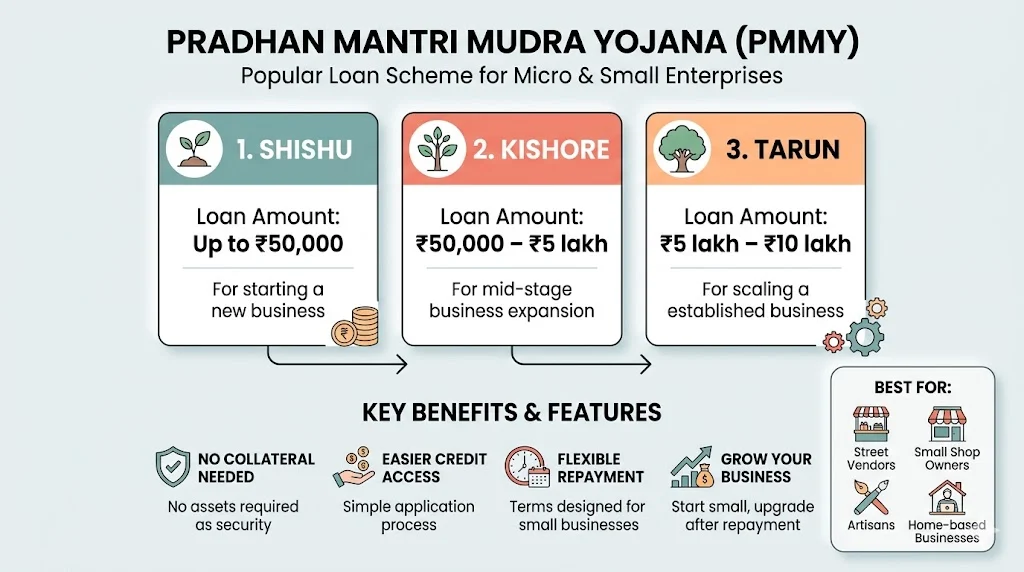

1.Pradhan Mantri Mudra Yojana (PMMY)

This is the most popular scheme right now.

| Category | Loan Amount |

|---|---|

| Shishu | Up to ₹50,000 |

| Kishore | ₹50,000 – ₹5 lakh |

| Tarun | ₹5 lakh – ₹10 lakh |

Best for: Small businesses, shop owners, freelancers

Use Tool: PM Mudra Loan EMI Calculator

No collateral needed. Many people start small and then upgrade loans after repayment. This scheme is mainly designed for micro and small entrepreneurs who are either starting a new business or expanding an existing one. It is especially useful for street vendors, small shop owners, service providers, artisans, and even home-based businesses. First-time entrepreneurs who don’t have assets to offer as security can benefit the most from this scheme.

One of the biggest advantages is that it provides easy access to credit without the burden of collateral. The interest rates are generally lower compared to private lenders, and the repayment terms are flexible, making it easier for small business owners to manage their finances. Another key benefit is the structured loan categories, which allow borrowers to grow step by step. You can start with a smaller loan under Shishu and gradually move to Kishore and Tarun as your business expands.

Additionally, the application process is relatively simple and can be done through banks, NBFCs, or even online platforms. Many banks also provide guidance and support during the process, which helps new entrepreneurs avoid confusion. Overall, this scheme acts as a strong financial foundation for anyone looking to build or scale a small business in India.

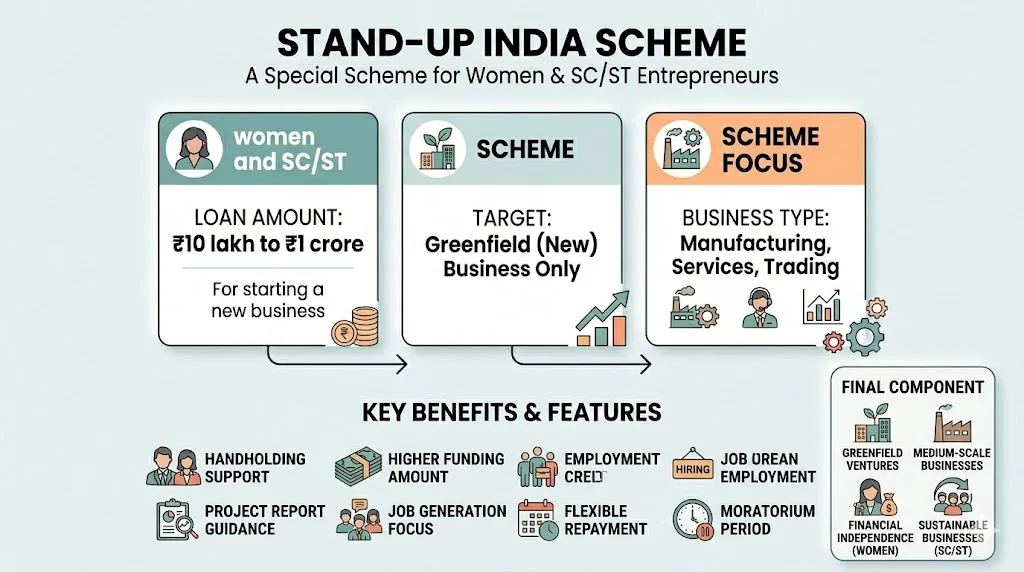

2. Stand-Up India Scheme

Focused on inclusivity.

- Loan: ₹10 lakh to ₹1 crore

- Target: Women and SC/ST entrepreneurs

- Business type: New ventures only

Tool: Stand Up India Scheme EMI Calculator – Empowering Entrepreneurs with Smart Planning

This scheme is mainly designed for first-time entrepreneurs from underrepresented groups who want to start a greenfield (new) business. It is especially useful for women who want financial independence and for SC/ST individuals looking to build sustainable businesses in sectors like manufacturing, services, or trading.

One of the biggest benefits of the Stand-Up India Scheme is that it provides not just funding but also handholding support. Banks often guide applicants through the process of setting up the business, preparing a project report, and understanding financial management. This makes it easier for beginners who may not have prior business experience.

Another key advantage is the relatively higher loan amount compared to schemes like Mudra, which allows entrepreneurs to start medium-scale businesses instead of very small setups. The scheme also encourages job creation, as businesses funded under it are expected to generate employment.

Additionally, repayment terms are flexible, and there is a moratorium period, giving businesses time to stabilize before starting repayments. This reduces financial pressure in the early stages. Good option if you’re starting something serious and need higher funding.

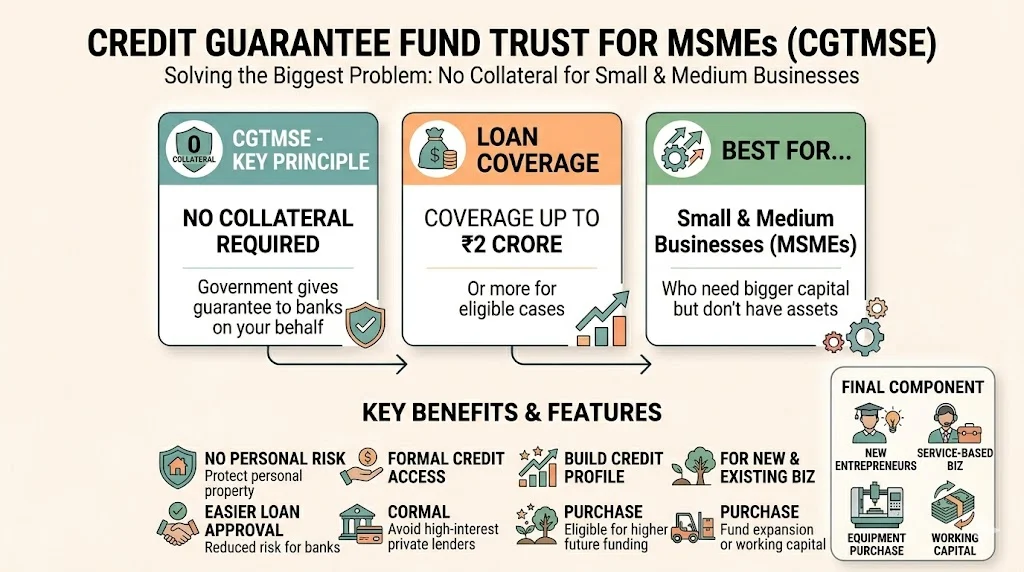

3. Credit Guarantee Fund Trust For MSMEs (CGTMSE)

This one solves the biggest problem, no collateral.

- Loan coverage up to ₹2 crore or more

- Government gives guarantee to banks

Best for: MSMEs who need bigger capital but don’t have assets

The CGTMSE scheme is mainly designed for small and medium businesses that struggle to provide security or property as collateral. It is especially useful for first-time entrepreneurs, service-based businesses, and manufacturing units that need funding to expand operations, purchase equipment, or manage working capital. Even existing MSMEs looking to scale up can benefit from this scheme without risking personal assets.

One of the biggest advantages is the government-backed guarantee, which reduces the risk for banks and increases your chances of loan approval. This means you can focus more on growing your business instead of worrying about pledging property. The scheme also supports both new and existing businesses, making it flexible for different stages of growth.

Another key benefit is easier access to formal credit, which helps businesses avoid high-interest private lenders. With proper repayment, businesses can build a strong credit profile and become eligible for higher funding in the future. Overall, CGTMSE acts as a strong support system for entrepreneurs who have ideas and potential but lack financial backing.

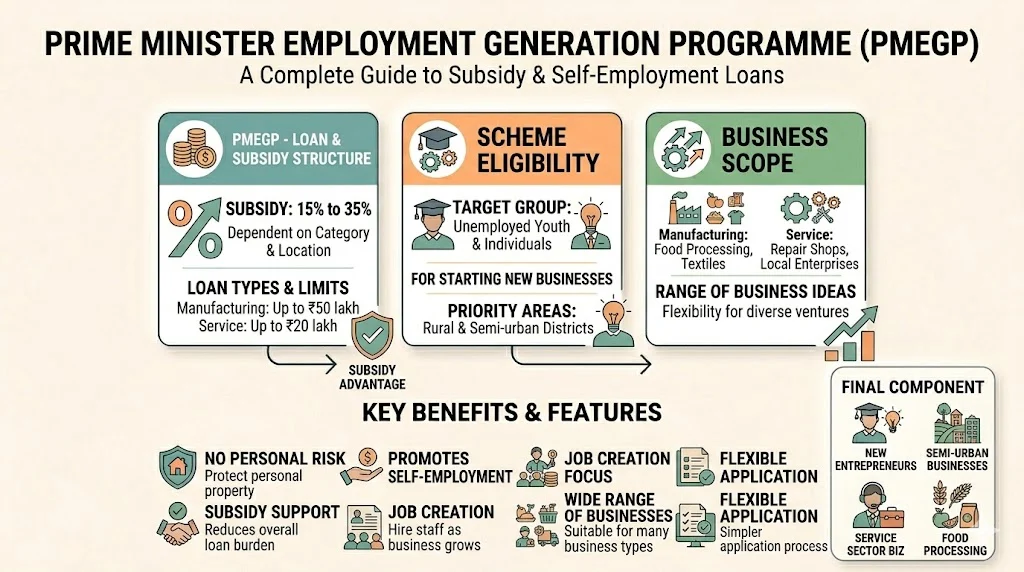

4. Prime Minister Employment Generation Programme (PMEGP)

Perfect for people starting from scratch.

- Subsidy: 15% to 35%

- Loan: Up to ₹50 lakh (manufacturing)

You basically get a part of your loan as subsidy. Huge advantage. This scheme is mainly for unemployed youth, aspiring entrepreneurs, and individuals who want to start a new business in manufacturing or service sectors. It is especially helpful for people in rural and semi-urban areas who may not have access to large capital or financial backing.

One of the biggest benefits is the subsidy support, which reduces the overall loan burden. Depending on your category and location, you can get a higher subsidy, making it easier to manage repayments. The scheme also encourages self-employment, helping people create their own income source instead of relying on jobs.

Another advantage is that it supports a wide range of business ideas, from small manufacturing units to service-based businesses like repair shops, food processing, and local enterprises. This flexibility makes it suitable for different types of entrepreneurs.

Additionally, the scheme promotes job creation. When your business grows, you can employ others, contributing to the local economy. Overall, PMEGP is a strong option if you want to start small but aim to build something sustainable over time.

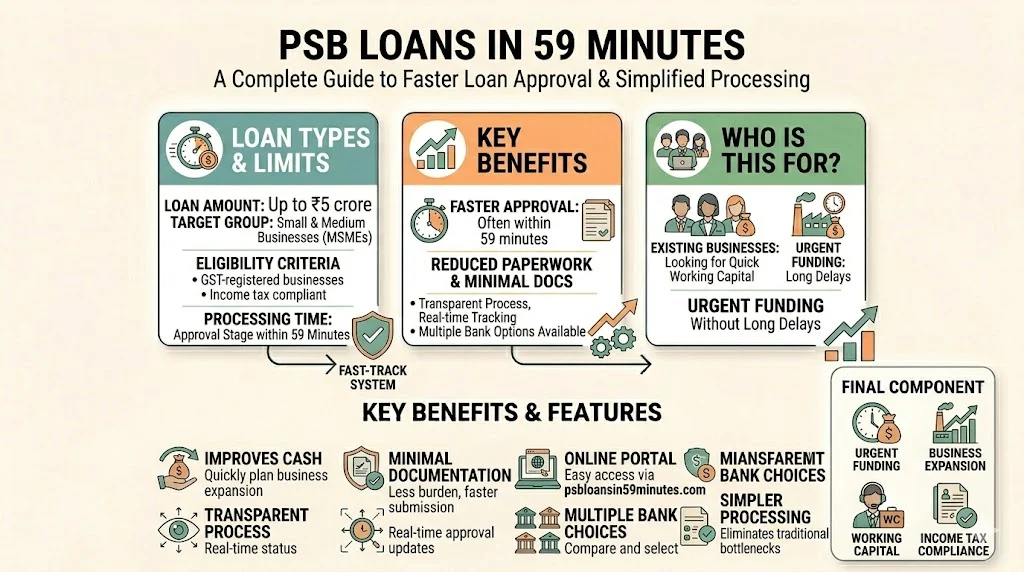

5. PSB Loans In 59 Minutes

Speed matters.

- Quick online approval

- For MSMEs and businesses

- Reduces paperwork and processing time

Not exactly a scheme but a fast-track system for loans.

Who Is This For?

- Small and medium business owners (MSMEs)

- Existing businesses looking for quick working capital

- Entrepreneurs who need urgent funding without long delays

- Startups with basic financial records

Key Benefits

- Faster loan approval, often within 59 minutes

- Minimal documentation compared to traditional loans

- Multiple bank options available in one platform

- Transparent process with real-time tracking

- Helps improve cash flow quickly

Additional Details

| Feature | Details |

|---|---|

| Loan Amount | Up to ₹5 crore |

| Processing Time | Within 59 minutes (approval stage) |

| Eligibility | GST-registered businesses, income tax compliant |

| Platform | Online portal (psbloansin59minutes.com) |

This system is especially useful for business owners who cannot afford long waiting periods. While final disbursement may take a few days, the quick approval gives clarity and confidence to plan business expansion or manage urgent financial needs.

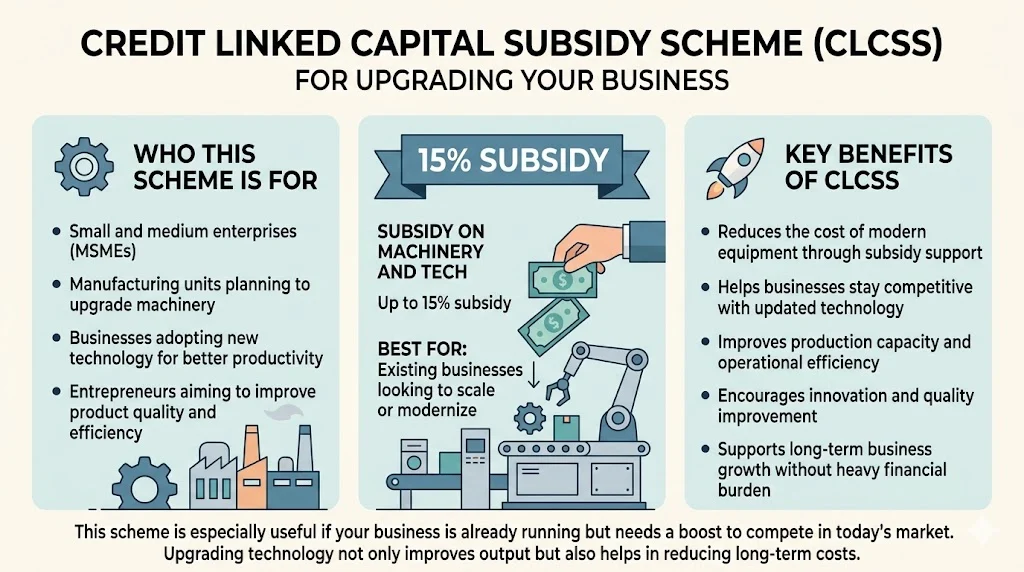

6. Credit Linked Capital Subsidy Scheme (CLCSS)

For upgrading your business.

- Subsidy on machinery and tech

- Up to 15% subsidy

Best for: Existing businesses looking to scale or modernize

Who This Scheme Is For

- Small and medium enterprises (MSMEs)

- Manufacturing units planning to upgrade machinery

- Businesses adopting new technology for better productivity

- Entrepreneurs aiming to improve product quality and efficiency

Key Benefits Of CLCSS

- Reduces the cost of modern equipment through subsidy support

- Helps businesses stay competitive with updated technology

- Improves production capacity and operational efficiency

- Encourages innovation and quality improvement

- Supports long-term business growth without heavy financial burden

Quick Overview

| Feature | Details |

|---|---|

| Target Group | MSMEs and small manufacturers |

| Subsidy | Up to 15% on eligible machinery |

| Purpose | Technology and equipment upgrade |

| Benefit | Lower investment cost and higher productivity |

This scheme is especially useful if your business is already running but needs a boost to compete in today’s market. Upgrading technology not only improves output but also helps in reducing long-term costs.

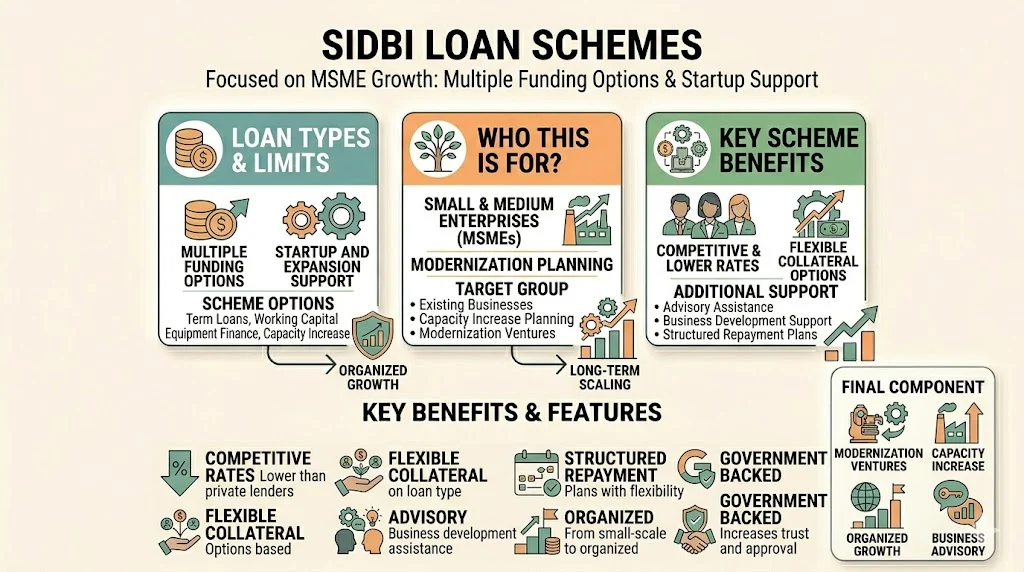

7. SIDBI Loan Schemes

Focused on MSME growth.

- Multiple funding options

- Startup and expansion support

Good if you’re serious about long-term scaling.

Who This Scheme Is For

- Small and Medium Enterprises (MSMEs) looking to expand operations

- Startups needing structured financial support

- Existing businesses planning modernization or capacity increase

- Entrepreneurs in manufacturing, services, or export sectors

Key Benefits Of SIDBI Loan Schemes

| Feature | Details |

|---|---|

| Loan Types | Term loans, working capital, equipment finance |

| Interest Rates | Competitive and often lower than private lenders |

| Collateral | Flexible options depending on loan type |

| Support | Advisory and business development assistance |

| Repayment | Structured repayment plans with flexibility |

Why It Stands Out

- Helps businesses move from small-scale to organized growth

- Offers sector-specific funding (like green energy, tech, exports)

- Backed by government, increasing trust and approval chances

If you’re planning long-term growth and want structured financial backing, SIDBI schemes can be a strong option to consider.

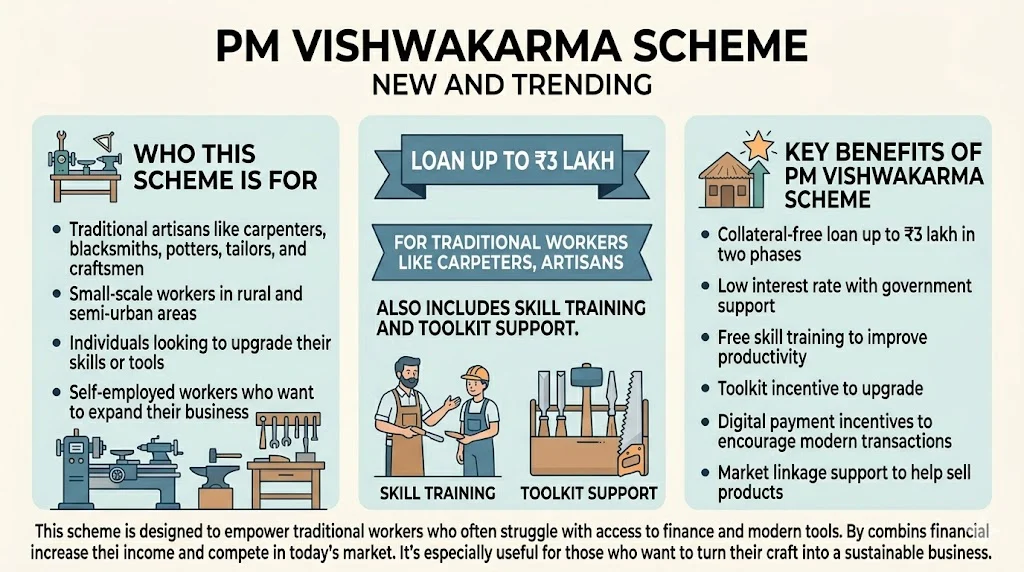

8. PM Vishwakarma Scheme

This scheme is New and trending.

- For traditional workers like carpenters, artisans

- Loan up to ₹3 lakh

Also includes skill training and toolkit support.

Who This Scheme Is For

- Traditional artisans like carpenters, blacksmiths, potters, tailors, and craftsmen

- Small-scale workers in rural and semi-urban areas

- Individuals looking to upgrade their skills or tools

- Self-employed workers who want to expand their business

Key Benefits Of PM Vishwakarma Scheme

- Collateral-free loan up to ₹3 lakh in two phases

- Low interest rate with government support

- Free skill training to improve productivity

- Toolkit incentive to upgrade equipment

- Digital payment incentives to encourage modern transactions

- Market linkage support to help sell products

Why It Matters

This scheme is designed to empower traditional workers who often struggle with access to finance and modern tools. By combining financial support with skill development, it helps artisans increase their income and compete in today’s market. It’s especially useful for those who want to turn their craft into a sustainable business.

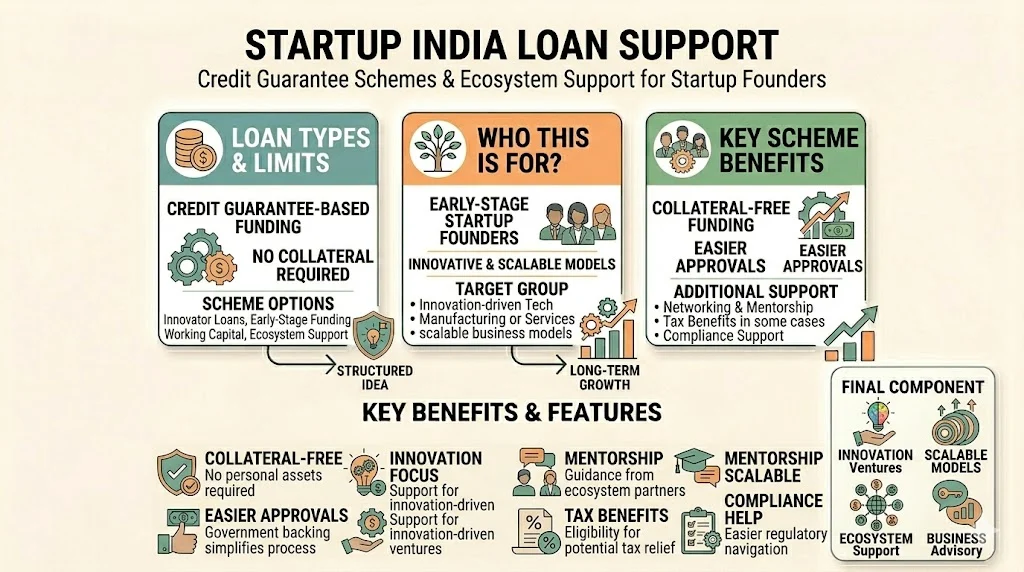

9. Startup India Loan Support

This scheme is For startup founders.

- Credit guarantee schemes

- Funding through ecosystem support

Works well if you have a structured business idea.

Who This Scheme Is For

- Early-stage startup founders with innovative ideas

- Entrepreneurs in tech, manufacturing, or service sectors

- Individuals with scalable business models

- Founders looking for government-backed financial support

Key Benefits Of Startup India Loan Support

- Access to collateral-free funding through credit guarantee

- Easier loan approvals due to government backing

- Support for innovation-driven businesses

- Networking and mentorship through startup ecosystem

- Tax benefits and compliance support in some cases

Quick Overview

| Feature | Details |

|---|---|

| Target Audience | Startup founders and innovators |

| Loan Type | Credit guarantee-based funding |

| Collateral | Not required in most cases |

| Support | Financial + ecosystem + mentorship |

| Best For | Scalable and structured business ideas |

This scheme is ideal if you’re serious about building a startup and need both funding and ecosystem support to grow faster.

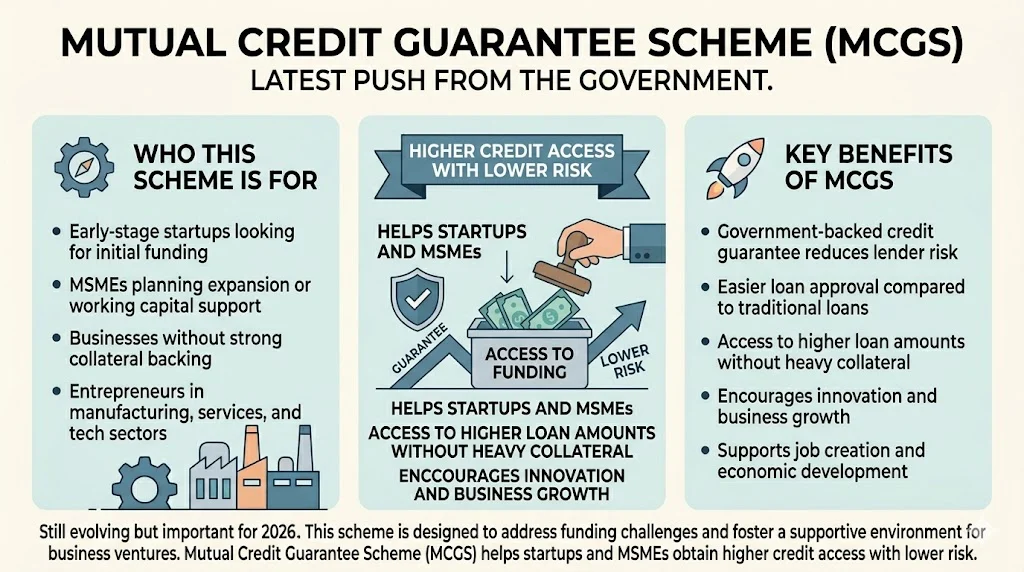

10. Mutual Credit Guarantee Scheme (MCGS)

Latest push from the government.

- Helps startups and MSMEs

- Higher credit access with lower risk

Who This Scheme Is For

- Early-stage startups looking for initial funding

- MSMEs planning expansion or working capital support

- Businesses without strong collateral backing

- Entrepreneurs in manufacturing, services, and tech sectors

Key Benefits

- Government-backed credit guarantee reduces lender risk

- Easier loan approval compared to traditional loans

- Access to higher loan amounts without heavy collateral

- Encourages innovation and business growth

- Supports job creation and economic development

Quick Overview

| Feature | Details |

|---|---|

| Target Audience | Startups & MSMEs |

| Loan Type | Credit guarantee-based funding |

| Collateral | Minimal or not required |

| Purpose | Expansion, working capital, new ventures |

| Advantage | Lower risk for banks, higher approval chances |

Still evolving but important for 2026.

Real Benefits That People Actually Care About

Let’s not talk theory. Here’s what actually matters when applying:

- No collateral in most schemes

- Lower interest rates compared to private loans

- Flexible repayment options

- Subsidies in some schemes

- Government backing increases approval chances

This is why these schemes are becoming popular even in small towns.

Public Opinion: What People Are Saying

Based on recent discussions and trends, the sentiment is mostly positive. Many people shared real success stories. One example mentioned a woman who started with a ₹2 lakh loan and later scaled to ₹9.5 lakh. Now she employs 10 to 15 people. That’s real impact. Bank campaigns also highlight cases like:

- Tailors turning into boutique owners

- Vendors expanding into branded businesses

- Farmers building agri-based startups

At the same time, not everything is perfect. Some users reported:

- Portal glitches in schemes like street vendor loans

- Delays in loan upgrades

- Confusion about eligibility

Still, overall trust in these schemes is quite strong. People see them as a genuine opportunity to grow.

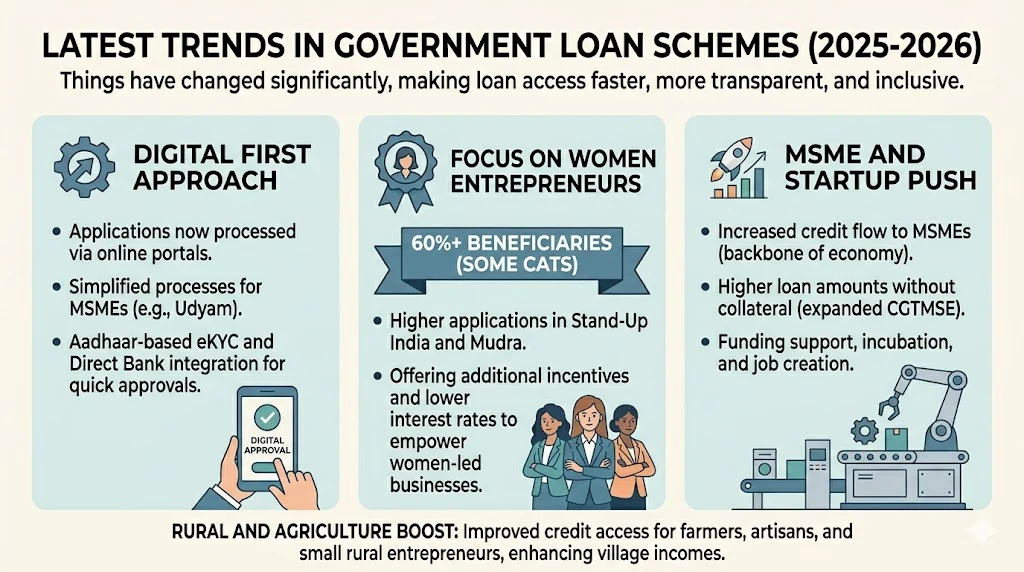

Latest Trends In Government Loan Schemes (2025-2026)

Things have changed significantly in the last couple of years, especially with the government focusing on making loan access faster, more transparent, and inclusive. Here’s a deeper look at the latest trends shaping government loan schemes in 2025–2026:

1) Digital First Approach

The biggest shift is the move towards a fully digital ecosystem. Most government loan applications are now processed through online portals, reducing paperwork and human dependency. Platforms like PSB Loans in 59 Minutes and Udyam Registration have simplified the process for MSMEs. Aadhaar-based eKYC, PAN verification, and direct bank integration have made approvals quicker and more secure. This also reduces corruption and middlemen involvement, which was a major issue earlier.

2) Focus On Women Entrepreneurs

There is a strong push to empower women-led businesses. Schemes like Stand-Up India and Mudra are seeing a higher percentage of female applicants. In fact, in some categories, women account for over 60% of beneficiaries. The government is also offering additional incentives, lower interest rates, and easier eligibility criteria to encourage more women to start and scale businesses. This shift is helping create financial independence and boosting local economies.

3) MSME And Startup Push

MSMEs are the backbone of India’s economy, and the government is actively increasing credit flow to this sector. Credit guarantee limits under schemes like CGTMSE have been expanded, allowing businesses to access higher loan amounts without collateral. Startups are also benefiting from improved funding support through Startup India initiatives, incubation programs, and easier compliance norms. This is encouraging innovation and job creation across industries.

4) Rural And Agriculture Boost

Rural development is another major focus area. Loan schemes are now closely linked with agriculture, food processing, and rural infrastructure projects. Farmers, artisans, and small rural entrepreneurs are getting better access to credit, training, and subsidies. This is not only improving income levels in villages but also reducing migration to cities by creating local employment opportunities.

Step-By-Step: How To Apply For Government Loan

If you’re serious about applying, follow this:

- Choose the right scheme based on your business

- Prepare documents

- Aadhaar

- Bank details

- Business plan (for larger loans)

- Apply via bank or official portal

- Wait for verification and approval

- Track your repayment properly

Simple, but many people skip preparation and face rejection.

Common Mistakes To Avoid

This is important, and honestly this is where most people go wrong even after choosing the right scheme.

- Applying without understanding eligibility: Many applicants rush into schemes like Mudra or PMEGP without checking basic criteria. For example, PMEGP requires a proper project report, and Stand-Up India is only for new ventures. Always read guidelines carefully before applying.

- No clear business plan: This is a big mistake, especially for schemes like CGTMSE or Startup India. Banks want to see how you will use the money and how you plan to repay it. Even a simple, realistic plan increases your chances a lot.

- Ignoring repayment discipline: People often think government loans are “easy money,” but missing EMIs can block future loan upgrades. In schemes like Mudra, timely repayment helps you move from Shishu to Kishore or Tarun category.

- Depending fully on agents: Some agents charge high fees or give wrong information. It’s better to apply directly through official portals or banks. Always verify details yourself.

- Not keeping documents ready: Missing documents like Aadhaar, bank statements, or business proof can delay approval. In schemes like PSB Loans in 59 Minutes, incomplete data can even lead to rejection.

Keep it clean and simple. Banks prefer genuine applicants who understand their business and responsibilities.

My Final Thoughts

Government loan schemes in India are not just policies on paper. They’re real chances that can genuinely change your situation if you use them wisely.

If you’re thinking about starting something, don’t wait for the “perfect” moment. Start small, learn as you go, and stay consistent. Many people you see running successful businesses today began with a small loan and a simple idea. What made the difference was patience and discipline, especially when it came to repayments.

My honest advice? Don’t overcomplicate things. Pick one scheme that fits your situation, take that first step, and keep moving forward. Growth doesn’t happen overnight, but it does happen if you stay committed. And if this guide helped you even a little, share it with someone who might need it. Sometimes, the right information at the right time can change everything.

Related Posts :

![[Long Term] Tech & Telecom Stocks In India For Future Investment](https://personalloaneligibilitycalculator.in/wp-content/uploads/Long-Term-Tech-Telecom-Stocks-In-India-For-Future-Investment.webp)

Share This Post