Best Defence Stocks In India 2026: Top 10 High-Growth Picks You Shouldn’t Ignore

Best Defence Stocks In India 2026: Top 10 High-Growth Picks You Shouldn’t Ignore

India’s defence sector is no longer a silent player. It has turned into one of the hottest themes in the stock market right now. With strong government push, rising geopolitical tensions, and massive budget allocation, defence stocks are getting serious attention from investors.

If you have been searching for the best defence stocks in India 2026 then you are not alone. Many investors are trying to figure out which companies can actually deliver long-term growth and not just short-term hype. And honestly, most articles out there just list names without giving real clarity.

In this blog post you will get list of important defence stock along with financial snapshot and share price target. So keep reading..

Table of Contents

Key Takeaways

- Defence sector is driven by government spending and long-term contracts

- Budget 2026 boosted visibility with ~17% increase in allocation

- Strong growth expected due to Atmanirbhar Bharat and export targets

- PSU + private players both are benefiting

- Stocks like HAL, BEL, BDL and Data Patterns are market favorites

- Sector has long-term potential but short-term volatility exists

Why Defence Stocks Are Trending In 2026

The biggest reason behind this rally is simple sustained and aggressive government spending combined with long-term strategic planning.

India’s defence budget has seen a consistent upward trend over the past few years, and in 2026 it has crossed ₹2.3 lakh crore for capital expenditure alone. This is not just a number on paper. It directly translates into large-scale contracts for fighter jets, naval vessels, missile systems, surveillance equipment, and advanced electronics. Companies with strong execution capabilities and existing government relationships are the biggest beneficiaries of this spending cycle.

Another major driver is the Atmanirbhar Bharat initiative. The government has clearly shifted its focus from importing defence equipment to building a self-reliant ecosystem within India. Several items have already been placed under the “negative import list,” meaning they must be sourced domestically. This policy shift is creating a massive opportunity for Indian manufacturers, both public and private, to scale operations and improve technological capabilities.

In addition to domestic demand, exports are emerging as a powerful growth engine. India is actively positioning itself as a global defence supplier, especially to friendly nations in Asia, Africa, and the Middle East. The government has set an ambitious target of ₹50,000 crore in defence exports by FY29. This opens up new revenue streams for companies and reduces dependence on domestic orders.

Moreover, geopolitical tensions and the need for modernization are accelerating procurement cycles. India is investing heavily in next-generation technologies like drones, electronic warfare systems, and AI-driven defence solutions. This ensures that the growth in the sector is not just cyclical but structural and long-term.

Top 10 Defence Stocks In India You Should Know

Here are the most important defence companies dominating the sector right now:

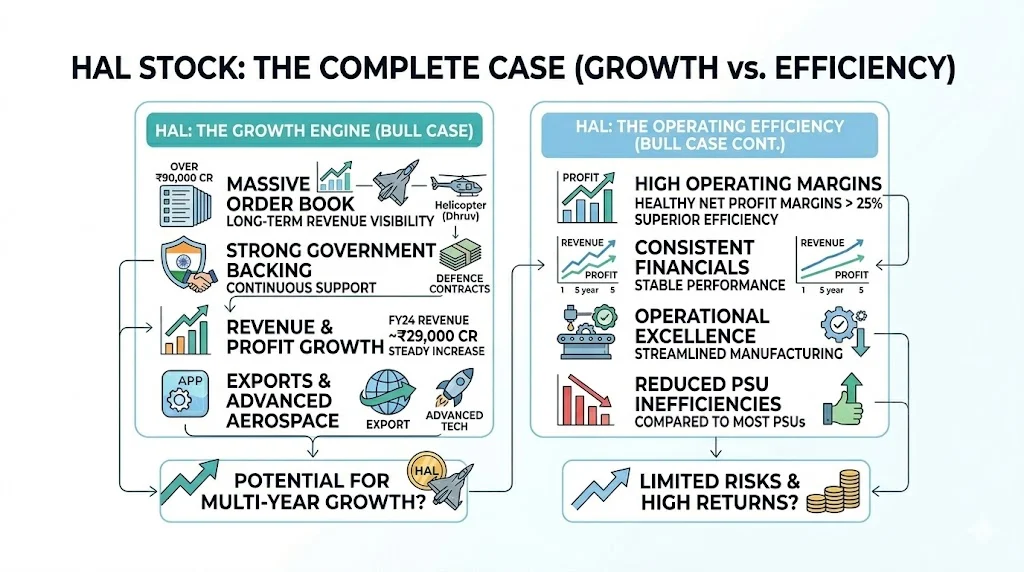

1. Hindustan Aeronautics Limited

This is the backbone of India’s aerospace sector. It manufactures Tejas fighter jets, helicopters like Dhruv and Rudra, and plays a key role in India’s indigenous defence programs.

In recent years, the company has shown strong financial performance. Its order book has crossed ₹90,000 crore, providing long-term revenue visibility. Revenue has been growing steadily, with FY24 revenue around ₹29,000 crore and net profit margins remaining healthy at over 25%.

- Massive order book ensuring multi-year growth visibility

- Strong government backing with continuous defence contracts

- High operating margins compared to most PSUs

- Consistent revenue and profit growth over the last 5 years

- Increasing focus on exports and advanced aerospace technologies

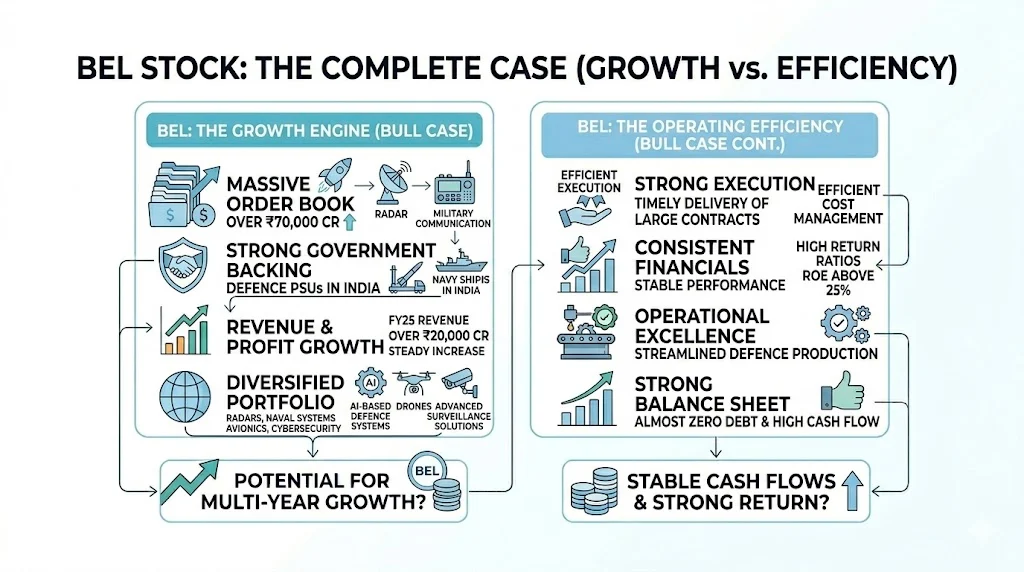

2. Bharat Electronics Limited

BEL is leading in radars, communication systems, and electronic warfare, making it one of the most reliable defence PSUs in India. In recent years, the company has shown strong financial performance with consistent revenue growth and improving margins. For FY25, BEL reported revenue of over ₹20,000 crore with a healthy net profit margin of around 18–20%, reflecting efficient cost management and strong order execution.

One of the biggest strengths of BEL is its massive order book, which stands above ₹70,000 crore, providing clear revenue visibility for the next few years. The company also maintains a strong balance sheet with almost zero debt and high return ratios, including ROE above 25%, which is impressive for a PSU.

- Strong execution with timely delivery of large defence contracts

- Diversified portfolio across radars, naval systems, avionics, and cybersecurity

- High demand driven by modernization of armed forces and indigenous defence push

- Increasing export opportunities in Southeast Asia and Africa

- Consistent dividend-paying stock with stable cash flows

BEL is also investing in future technologies like AI-based defence systems, drones, and advanced surveillance solutions, which positions it well for long-term growth in modern warfare.

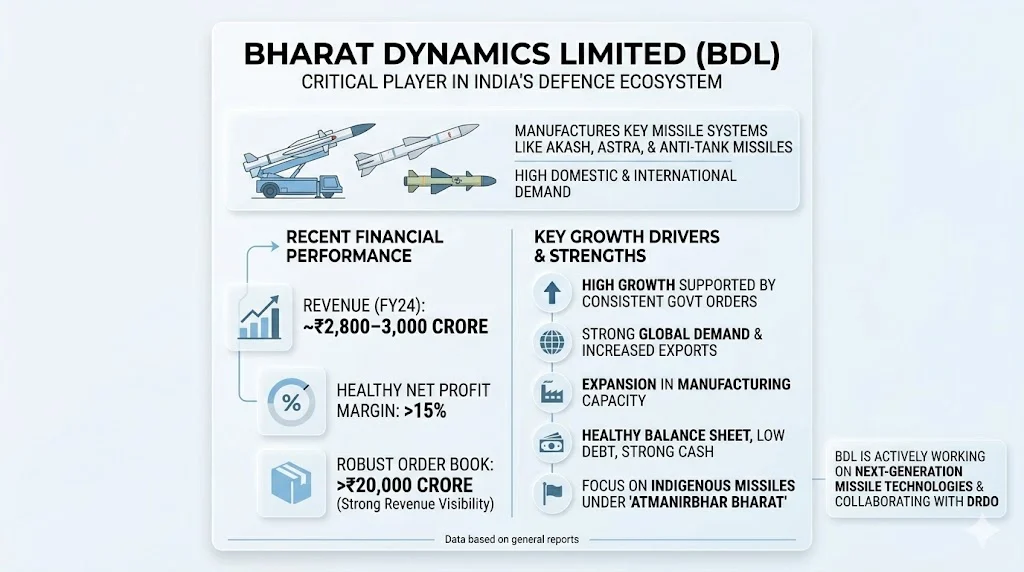

3. Bharat Dynamics Limited

BDL focuses on missiles and underwater weapons, making it a critical player in India’s defence ecosystem. The company manufactures key missile systems like Akash, Astra, and anti-tank guided missiles, which are in high demand both domestically and internationally.

In recent financial performance, Bharat Dynamics Limited has shown strong growth. For FY24, the company reported revenue of around ₹2,800–3,000 crore with a healthy net profit margin of over 15%. Its order book remains robust, estimated at over ₹20,000 crore, providing strong revenue visibility for the next few years.

- High growth trajectory supported by consistent government orders

- Strong demand globally as India increases defence exports

- Expansion in manufacturing capacity to meet rising production needs

- Healthy balance sheet with low debt and strong cash reserves

- Increasing focus on indigenous missile systems under Atmanirbhar Bharat

Additionally, BDL is actively working on next-generation missile technologies and collaborating with DRDO, which strengthens its long-term growth potential. The company’s strategic importance, combined with rising geopolitical tensions and export opportunities, makes it one of the most promising defence stocks in India.

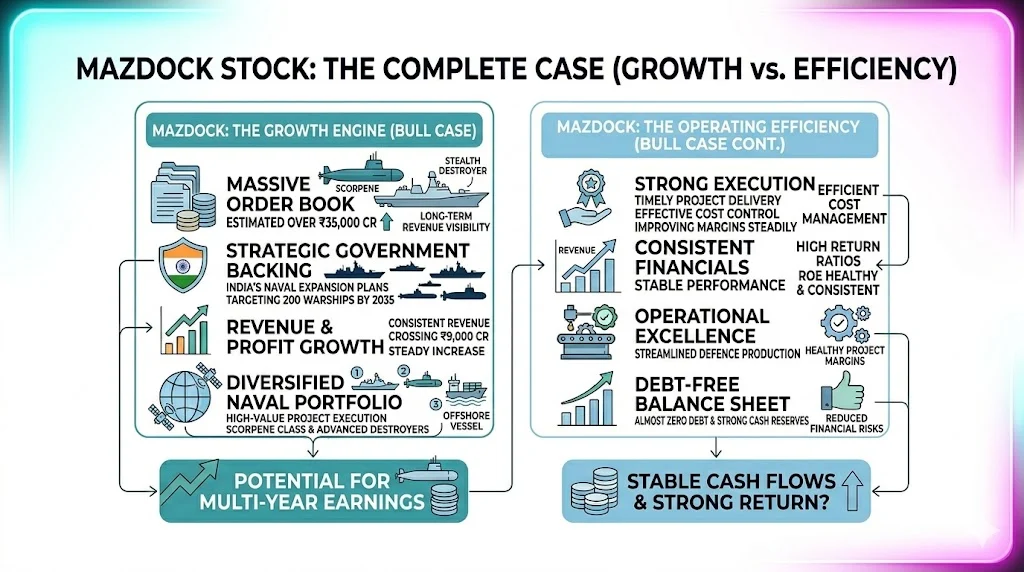

4. Mazagon Dock Shipbuilders Limited

Key player in submarines and warships, Mazagon Dock Shipbuilders has emerged as one of the most strategically important defence PSUs in India. The company is currently executing high-value projects like Scorpene-class submarines and advanced stealth destroyers, which ensures long-term revenue visibility.

In recent financials, the company has shown strong growth with revenue crossing ₹9,000 crore and net profit margins improving steadily due to better execution and cost control. Its order book remains robust, estimated at over ₹35,000 crore, providing multi-year earnings visibility.

- Strong order pipeline backed by government contracts

- Beneficiary of India’s naval expansion plans targeting 200 warships by 2035

- High operating margins compared to peers

- Debt-free balance sheet with strong cash reserves

- Increasing focus on export opportunities in Southeast Asia and Africa

The company’s fundamentals are solid, with a healthy return on equity (ROE) and consistent dividend payouts, making it attractive for long-term investors. Its strategic importance in India’s defence ecosystem ensures continuous government support, which reduces business risk compared to private players.

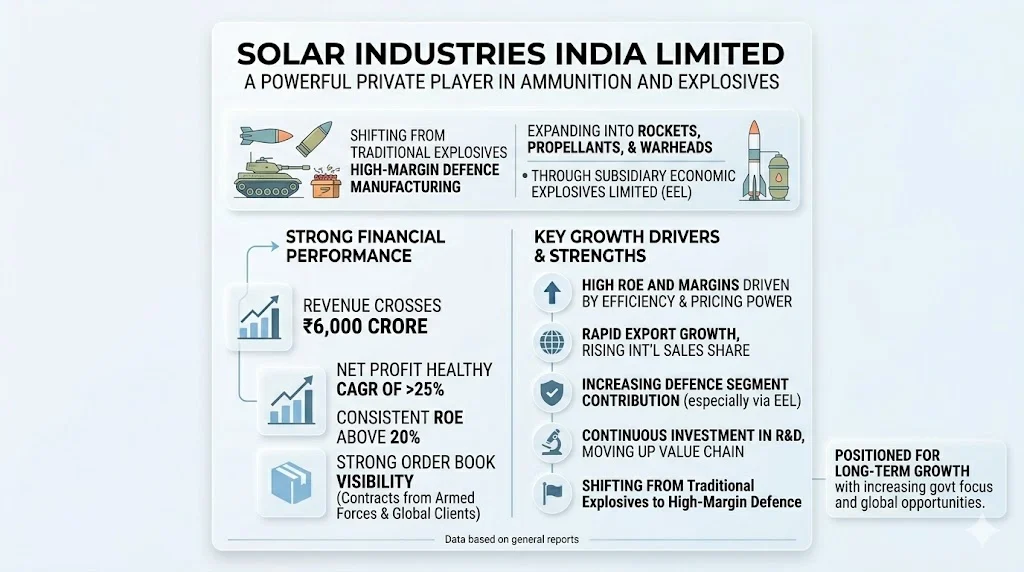

5. Solar Industries India Limited

A powerful private player in ammunition and explosives, Solar Industries has emerged as one of the fastest-growing defence-linked companies in India. In recent years, the company has shown strong financial performance, with revenue crossing ₹6,000 crore and net profit growing at a healthy CAGR of over 25%. Its return on equity (ROE) consistently stays above 20%, reflecting efficient capital utilization and strong profitability.

- High ROE and margins driven by operational efficiency and pricing power

- Rapid export growth, with international sales contributing a rising share of total revenue

- Increasing defence segment contribution, especially through its subsidiary Economic Explosives Limited (EEL)

- Strong order book visibility supported by contracts from Indian armed forces and global clients

- Expansion into advanced defence products like rockets, propellants, and warheads

- Continuous investment in R&D, helping the company move up the value chain

What makes Solar Industries particularly attractive is its shift from a traditional explosives business to a high-margin defence manufacturing player. With increasing government focus on indigenous ammunition production and export opportunities, the company is well-positioned for long-term growth.

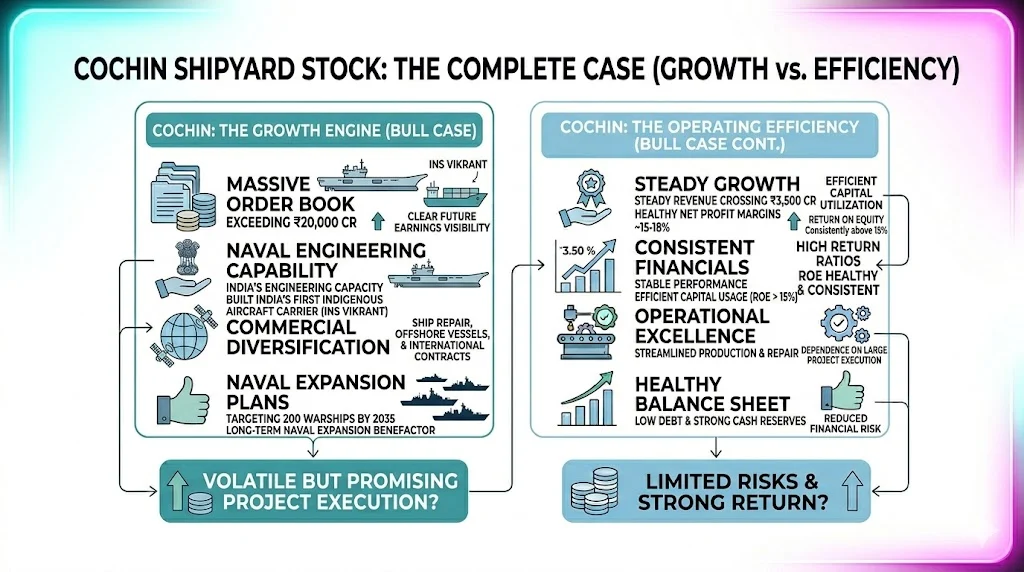

6. Cochin Shipyard Limited

Built India’s first indigenous aircraft carrier, INS Vikrant, which highlights its strong engineering capability and strategic importance in India’s naval expansion.

In recent financial performance, Cochin Shipyard has shown steady growth with revenue crossing ₹3,500 crore and net profit margins remaining healthy around 15–18%. The company also maintains a strong order book exceeding ₹20,000 crore, providing clear visibility for future earnings. Its return on equity (ROE) has been consistently above 15%, indicating efficient capital utilization.

- Strong naval projects with increasing government contracts for warships and repair services

- Commercial diversification into ship repair, offshore vessels, and international contracts

- Healthy balance sheet with low debt and strong cash reserves

- Beneficiary of India’s long-term naval expansion plans targeting 200 warships by 2035

- Volatile but promising due to cyclical nature and dependence on large project execution

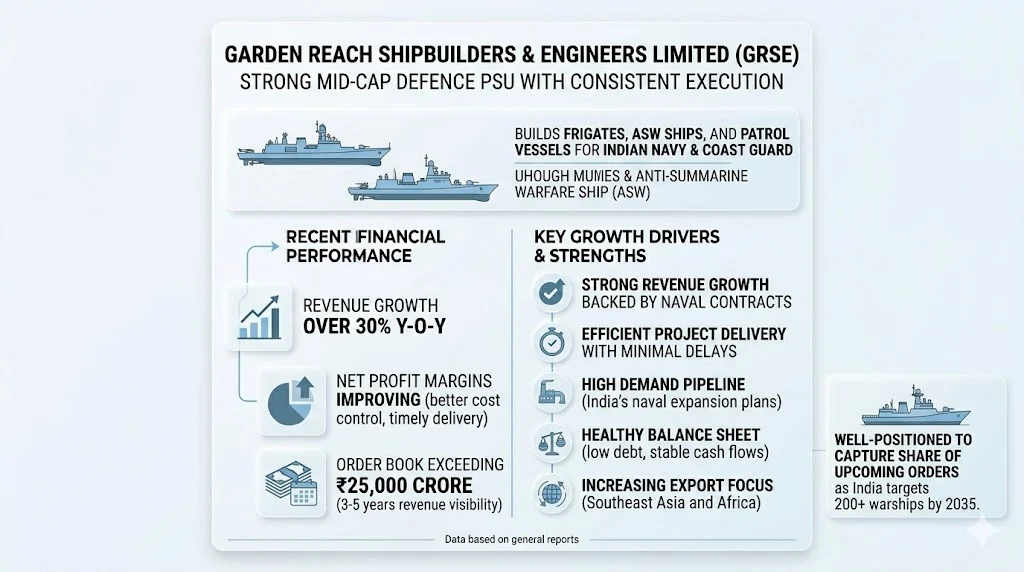

7. Garden Reach Shipbuilders & Engineers Limited

Known for building frigates, anti-submarine warfare ships, and advanced patrol vessels for the Indian Navy and Coast Guard, Garden Reach Shipbuilders & Engineers (GRSE) has emerged as a strong mid-cap defence PSU with consistent execution capabilities.

In recent financial performance, GRSE reported revenue growth of over 30% year-on-year, with net profit margins improving due to better cost control and timely project delivery. The company maintains a healthy order book exceeding ₹25,000 crore, providing strong revenue visibility for the next 3–5 years.

- Strong revenue growth backed by execution of large naval contracts

- Efficient project delivery with minimal delays compared to peers

- High demand pipeline driven by India’s naval expansion plans

- Healthy balance sheet with low debt and stable cash flows

- Increasing focus on export opportunities in Southeast Asia and Africa

Additionally, GRSE benefits from government initiatives aimed at strengthening indigenous shipbuilding capabilities. Its expertise in modular ship construction and advanced engineering gives it a competitive edge. With India targeting a fleet of over 200 warships by 2035, GRSE is well-positioned to capture a significant share of upcoming naval orders, making it a promising long-term player in the defence sector.

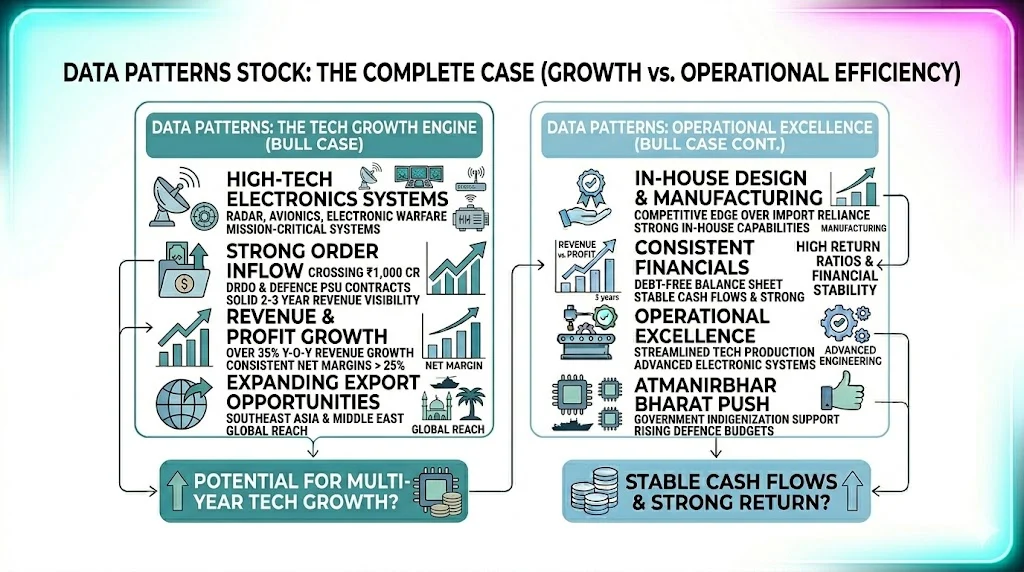

8. Data Patterns (India) Limited

One of the fastest-growing private defence tech companies in India, Data Patterns has built a strong reputation in indigenous defence electronics and mission-critical systems. In recent financials, the company reported revenue growth of over 35% year-on-year, with net profit margins consistently above 25%, reflecting strong operational efficiency. Its order book has crossed ₹1,000 crore, providing solid revenue visibility for the next 2–3 years.

- High-tech systems across radar, avionics, and electronic warfare

- Strong order inflow driven by DRDO and defence PSU contracts

- Export opportunities expanding in Southeast Asia and the Middle East

The company also maintains a debt-free balance sheet, which adds financial stability and reduces risk during market volatility. Its focus on in-house design and manufacturing gives it a competitive edge over peers who rely on imports.

Additionally, increasing government push for indigenization under Atmanirbhar Bharat is directly benefiting companies like Data Patterns. With rising defence budgets and growing demand for advanced electronics, the company is well-positioned for long-term growth.

9. Astra Microwave Products Limited

Specializes in radar and electronic warfare systems, making it a critical player in India’s defence electronics ecosystem. Astra Microwave has built strong capabilities in RF and microwave components used in missiles, radars, and communication systems.

In recent financial performance, the company reported revenue growth of around 20–25% year-on-year, with improving operating margins due to better execution and higher-value contracts. Its order book remains strong, supported by consistent inflows from DRDO, ISRO, and major defence PSUs like BEL and HAL.

- Niche segment with high entry barriers

- Low import dependence due to indigenous manufacturing

- Strong partnerships with DRDO, ISRO, and global OEMs

- Healthy order book ensuring revenue visibility

- Improving margins and steady cash flow generation

Additionally, Astra Microwave is expanding its presence in export markets, which could act as a major growth driver in the coming years. Its focus on advanced technologies like electronic warfare and space applications positions it well for long-term growth in both defence and aerospace sectors.

10. MTAR Technologies Limited

Supplies critical components for defence, space, and nuclear sectors, making it a strategically important player in India’s high-precision manufacturing ecosystem.

In recent years, MTAR Technologies has shown steady financial growth. The company reported revenue growth of around 20–25% CAGR over the last few years, with strong operating margins typically in the range of 25–30%. Its return on equity (ROE) has remained healthy, often above 20%, indicating efficient capital utilization.

- High precision engineering with niche capabilities in complex components

- Strong order book supported by long-term contracts with ISRO, DRDO, and global clients

- Multi-sector exposure including clean energy (fuel cells), space, and defence

- Asset-light model with high margin profile

- Increasing export contribution, especially from international space and defence programs

What makes MTAR stand out is its technological expertise and entry barriers. The company operates in segments where competition is limited due to strict quality standards and certifications. Its long-standing relationships with key institutions like ISRO and global OEMs provide strong revenue visibility.

Overall, MTAR Technologies is often considered a hidden gem because of its niche positioning, consistent financial performance, and strong growth potential in emerging sectors like space exploration and advanced defence systems.

Sector Growth Data (What Numbers Are Saying)

Here’s a quick breakdown of why this sector is attracting investors:

| Factor | Data |

|---|---|

| Budget Increase | ~17% growth |

| Export Target | ₹50,000 crore by FY29 |

| Production Growth | ~20% CAGR expected |

| Manufacturing Goal | ₹3 lakh crore by 2029 |

| Naval Target | 200 warships by 2035 |

This is not just hype. It’s a structural story backed by strong financials and real business growth. For example, companies like Hindustan Aeronautics Limited (HAL) reported revenue growth of over 15% year-on-year with a massive order book exceeding ₹80,000 crore, ensuring long-term visibility. Bharat Electronics Limited (BEL) continues to maintain healthy operating margins above 20% and has an order pipeline of more than ₹70,000 crore, reflecting consistent demand.

Private players are also showing strong fundamentals. Data Patterns has delivered revenue growth of around 30% CAGR in recent years, with improving net profit margins and increasing export opportunities. Similarly, Solar Industries has seen strong earnings growth driven by its defence segment, with ROE consistently above 20%, indicating efficient capital utilization.

Another key factor is the low debt levels across most defence companies, especially PSUs, which makes them financially stable even during market volatility. Additionally, rising government contracts and export orders are improving cash flows and reducing dependency on a single revenue stream.

These numbers clearly show that the defence sector is not driven by speculation alone. It is supported by strong balance sheets, consistent earnings growth, and long-term government-backed demand, making it a fundamentally solid investment theme.

Public Opinion (What People Are Saying On X)

The sentiment on X (Twitter) is mostly bullish.

- Many investors call defence stocks “long-term compounders”

- Stocks like BEL and Data Patterns are frequently trending

- Shipbuilding companies like Mazagon Dock and GRSE are getting attention

But not everything is perfect. Some users also pointed out corrections:

- Cochin Shipyard down ~40% from peak

- Mazagon Dock down ~38%

- BDL saw profit booking

Still, overall sentiment remains positive. Most people believe this is just a pause, not the end of the rally.

What Most Articles Miss (Important Insight)

Most competitor articles just list stocks. But they miss the bigger picture. Here’s what actually matters:

1. Order Book Visibility

Companies with strong order pipelines will perform better.

2. Tech Capability

Future belongs to companies working in:

- Drones

- AI systems

- Electronic warfare

- C4ISR systems

3. Private Sector Rise

Earlier only PSUs dominated. Now private companies are growing fast.

4. Export Potential

This is the real game changer. Companies with export exposure can grow faster.

Risks You Should Not Ignore

To be more real. This sector is not risk-free, and understanding the downside is just as important as spotting opportunities.

First, the biggest risk is heavy dependence on government spending. Defence companies in India rely largely on government contracts, which means their revenue visibility is tied to budget allocations and policy priorities. If there is any delay in approvals, tender processes, or fund disbursement, it can directly impact earnings and stock performance.

Second, policy changes can significantly influence the sector. While initiatives like Atmanirbhar Bharat are currently boosting domestic manufacturing, any shift in import policies, defence procurement rules, or geopolitical priorities can alter the growth trajectory of these companies. Investors need to stay updated with policy announcements and defence deals.

Another important factor is valuation risk. Many defence stocks have already seen sharp rallies over the past couple of years. As a result, some companies are trading at premium valuations compared to their historical averages. Buying at elevated levels without proper analysis can reduce future returns, especially if earnings growth does not match expectations.

Profit booking is also common in this sector. After strong rallies, stocks often witness corrections as investors lock in gains. This can create short-term volatility, even if the long-term story remains intact. For example, several defence stocks have already seen sharp pullbacks after hitting their peaks.

Lastly, execution risk should not be ignored. Defence projects are complex and long-term in nature. Delays in project completion, cost overruns, or technical challenges can affect company performance.

So instead of blindly jumping in, it’s better to take a balanced approach. Focus on fundamentally strong companies, invest gradually, and always keep a long-term perspective while managing risks carefully.

Final Thoughts

The Indian defence sector is definitely moving into a strong growth phase, and honestly, it’s exciting to watch. With government support, rising exports, and rapid technological changes, the opportunities here are real.

But if I can share one honest piece of advice don’t get carried away by the hype. Take your time. Look at the fundamentals. Try to understand which companies are actually building something meaningful for the future.

Personally, I would focus on businesses that have:

- Strong order books

- Proven execution

- Exposure to future technologies

Because in the long run, it’s not the noise that creates wealth it’s patience and smart decisions. So invest thoughtfully, stay consistent, and let time do its work.

Also Read: Subex Share Price Target 2026, 2027, 2028, 2029, 2030, 2040, 2050

Related Posts :

![[Long Term] Tech & Telecom Stocks In India For Future Investment](https://personalloaneligibilitycalculator.in/wp-content/uploads/Long-Term-Tech-Telecom-Stocks-In-India-For-Future-Investment.webp)

Share This Post