Hathway Share Price Target 2026, 2027 To 2050

Hathway Share Price Target

Hathway Cable & Datacom is one of the leading cable TV and broadband service providers in India. The company operates in digital cable television and high speed internet services. It serves millions of customers across major cities. The company provides services like cable TV distribution, broadband internet, and enterprise solutions. It is also backed by Reliance Group which gives strong promoter support.

In the last 5 years, the company has shown slow revenue growth of around 3% CAGR. Revenue increased from ₹1,732 crore in 2021 to ₹2,040 crore in 2025. However profit has been volatile. Net profit declined after 2021 and then showed slight recovery. ROE remains low at around 2–3% which shows limited efficiency. Promoter holding is stable at 75% which is a positive sign. The company is almost debt free which gives financial stability.

Table of Contents

Hathway Share Price Target 2026

| Month | Min Price | Max Price |

|---|---|---|

| Jan | ₹8 | ₹12 |

| Dec | ₹10 | ₹15 |

For 2026, the company is going through a weak phase in stock price. As of March 2026, the stock is trading near ₹9–₹10 levels and also touched 52 week lows. This shows strong selling pressure in the market.

One key update is the resignation of Senior VP Sales in March 2026. This is not a major negative but it shows internal changes in strategy. Also there are no big growth triggers like acquisitions or strong earnings growth recently.

The broadband and cable sector is facing high competition from Jio, Airtel and OTT platforms. This is affecting subscriber growth. Because of this, 2026 can remain a consolidation year for Hathway.

Hathway Share Price Target 2027

| Month | Min Price | Max Price |

|---|---|---|

| Jan | ₹8 | ₹12 |

| Dec | ₹10 | ₹15 |

In 2027, growth will depend on how the company improves its broadband business. Broadband is the future segment as cable TV is slowly declining.

The company is working on improving customer service and digital platforms like self care apps and automation tools. If customer complaints reduce and retention improves, revenue stability can come.

Regulatory changes by TRAI which will be implemented from April 2026 can also impact operations. These rules can increase compliance cost. If Hathway adapts well then it can improve margins slowly.

Hathway Share Price Target 2028

| Month | Min Price | Max Price |

|---|---|---|

| Jan | ₹8 | ₹12 |

| Dec | ₹10 | ₹15 |

By 2028, the company can benefit from rising internet usage in India. Demand for high speed broadband is increasing every year.

Hathway already has a strong network presence in many cities. If the company upgrades its infrastructure and provides better service quality, it can attract new customers.

However, competition will still remain high. So growth will not be very fast. The company needs to focus on innovation and customer satisfaction to stay relevant.

Hathway Share Price Target 2029

| Month | Min Price (₹) | Max Price (₹) |

|---|---|---|

| Jan | 8 | 12 |

| Dec | 10 | 15 |

In 2029, long term growth will depend on how well the company manages its business transition. Cable TV business is declining and broadband is growing.

If Hathway successfully shifts its focus towards broadband and enterprise services, then revenue growth can improve. Also if margins improve from current 4–5% levels, then profitability will increase. This can support share price growth.

Hathway Share Price Target 2030

| Month | Min Price | Max Price |

|---|---|---|

| Jan | ₹8 | ₹12 |

| Dec | ₹10 | ₹15 |

By 2030, the company may become more broadband focused. Digital consumption in India will be very high. If Hathway builds strong network quality and competitive pricing, it can survive in the market.

But if competition dominates, then growth can remain slow. Investors should track revenue growth and subscriber data carefully.

Hathway Share Price Target 2040

| Month | Min Price | Max Price |

|---|---|---|

| Jan | ₹8 | ₹12 |

| Dec | ₹10 | ₹15 |

For 2040, the company’s future depends on its ability to adapt to technology changes. The telecom and media sector will change rapidly. If Hathway invests in new technologies like fiber networks and digital platforms, then long term growth is possible.

Otherwise, the business can struggle due to outdated model. So long term investment depends on execution.

Hathway Share Price Target 2050

| Month | Min Price (₹) | Max Price (₹) |

|---|---|---|

| Jan | 8 | 12 |

| Dec | 10 | 15 |

By 2050, only strong and innovative companies will survive in this sector. If Hathway transforms into a strong broadband and digital service company, then it can create value. But if it fails to adapt, then growth can remain limited. So this stock is more suitable for high risk long term investors.

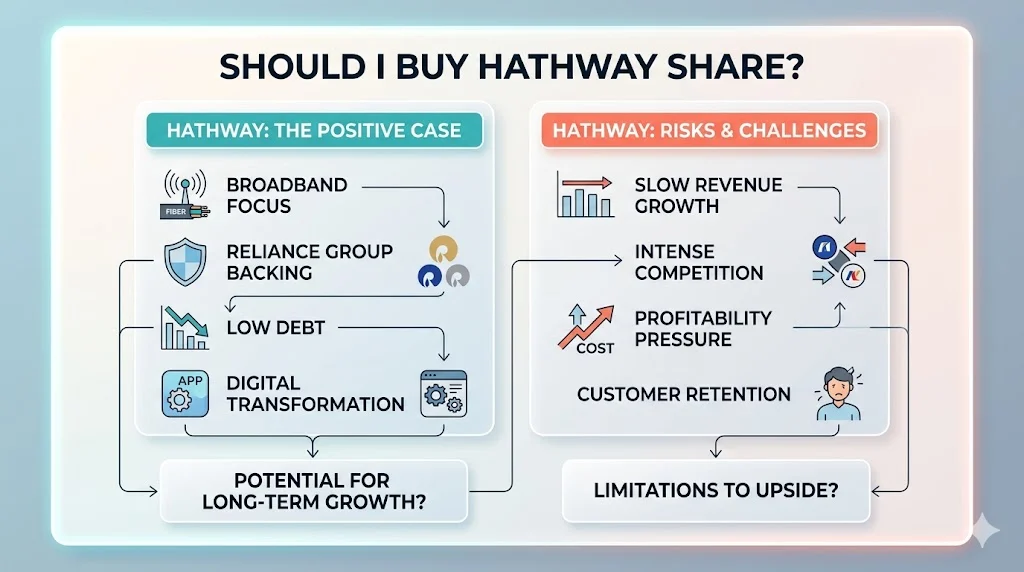

Should I Buy Hathway Share?

Hathway is increasingly shifting its focus toward broadband growth and digital transformation, which is a crucial step considering the declining relevance of traditional cable TV services. The company is working on strengthening its fiber network infrastructure and improving internet speeds to meet rising consumer demand. Additionally, it is investing in digital platforms such as self-service apps, automated customer support systems, and improved billing processes to enhance user experience and reduce operational inefficiencies.

One of the key strengths of Hathway is its strong promoter backing from the Reliance Group, which provides financial stability and strategic support. The company also maintains a low debt profile, which reduces financial risk and gives it flexibility to invest in future growth opportunities. These factors make the company fundamentally stable compared to many smaller players in the industry.

However, investors should also consider the challenges. Revenue growth has been relatively slow, and profitability remains under pressure due to intense competition from major telecom players like Jio and Airtel. These competitors are aggressively expanding their broadband services with better pricing, bundled offerings, and superior network quality. Hathway, on the other hand, has not shown aggressive expansion or innovation at the same pace, which could limit its market share growth.

Moreover, customer service issues and retention challenges have impacted the company’s brand perception in some regions. Without significant improvements in service quality and network reliability, it may struggle to attract and retain subscribers in the long term.

Therefore, while Hathway has some strong fundamentals, it also carries notable risks. Investors should carefully evaluate both the growth potential and competitive challenges before making any investment decision.

Is Hathway Stock Good to Buy (Bull Case & Bear Case)

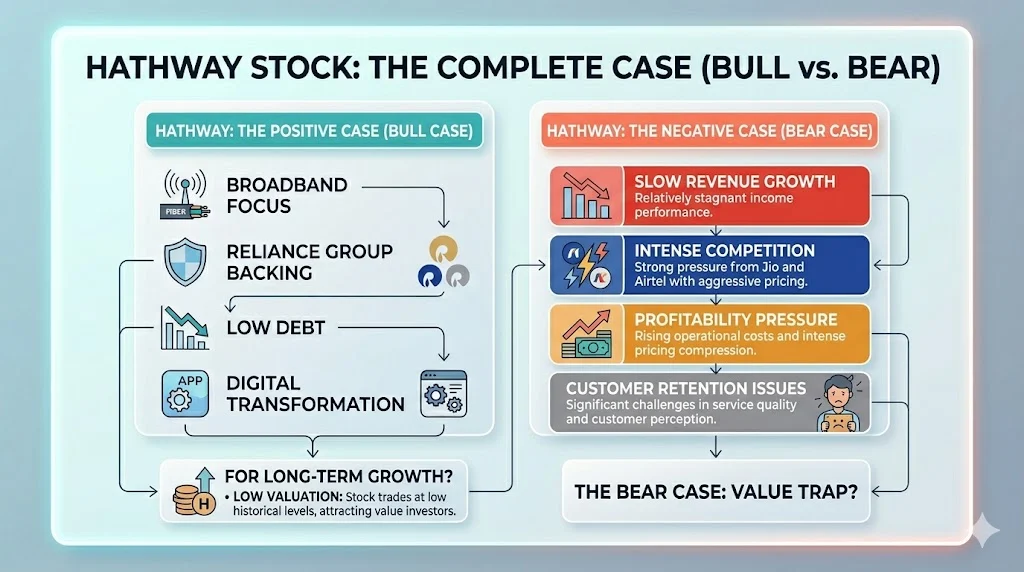

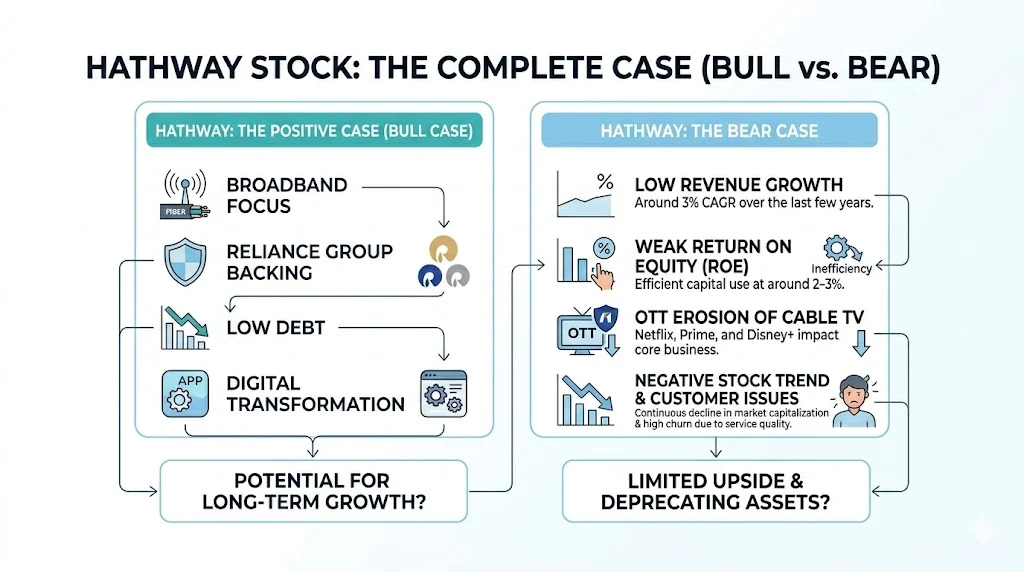

Bull Case:

Hathway Cable & Datacom Ltd has a few strong positives that can support long-term growth if executed properly. One of the biggest strengths is its strong promoter backing, with around 75% holding by Reliance Group. This provides financial stability and strategic support, which can help the company survive tough competition in the telecom and broadband sector.

The company is also almost debt-free, which reduces financial risk significantly. Low debt means lower interest burden and better flexibility to invest in future growth opportunities like network expansion and technology upgrades.

Another important factor is the rising demand for broadband services in India. With increasing digital consumption, work-from-home culture, online education, and OTT platforms, internet usage is growing rapidly. Hathway already has an established presence in multiple cities, which gives it an advantage to capture this demand if it improves service quality.

Additionally, the stock is currently trading at a low valuation compared to its historical levels. This can attract value investors who are looking for turnaround opportunities. If the company shows even moderate improvement in revenue and profitability, the stock can see re-rating in the market.

Bear Case:

Despite some positives, Hathway faces several serious challenges that investors should not ignore. The biggest concern is its very low revenue growth, which is around 3% CAGR over the last few years. This indicates that the company is struggling to expand its business in a highly competitive market.

Return on Equity (ROE) is also very weak at around 2–3%, which shows inefficient use of capital. Investors generally prefer companies with higher ROE, so this can limit investor interest in the stock.

The traditional cable TV business is declining due to the rise of OTT platforms like Netflix, Amazon Prime, and Disney+ Hotstar. This structural shift is negatively impacting Hathway’s core business segment.

The stock price trend has also been negative, reflecting weak investor confidence. Continuous decline in market capitalization shows that the market is not optimistic about near-term growth. Lastly, customer service issues and complaints have affected the company’s brand image. Poor service quality can lead to customer churn, which directly impacts revenue and long-term sustainability.

Promoters Holding Of Hathway

| Metric | Value |

|---|---|

| Promoter Holding | 75% |

Promoter holding is stable at 75%. This is a strong positive sign. It shows confidence of promoters in the business. High promoter holding also reduces volatility in stock.

Revenue Growth Of Hathway

| Year | Revenue (₹ Cr) | Growth |

|---|---|---|

| 2021 | 1,732 | – |

| 2022 | 1,793 | 3.5% |

| 2023 | 1,858 | 3.6% |

| 2024 | 1,981 | 6.6% |

| 2025 | 2,040 | 3.0% |

Revenue growth has remained modest, with a compound annual growth rate (CAGR) of approximately 3% over the observed period. As reflected in the table, revenue increased gradually from ₹1,732 crore in 2021 to ₹2,040 crore in 2025, indicating a steady but limited expansion trajectory.

While there was a slightly higher growth phase in 2024 at around 6.6%, the overall trend suggests inconsistency and lack of strong momentum. Compared to industry peers, especially in the rapidly evolving broadband and digital services sector, this level of growth falls below expectations.

The subdued revenue performance highlights the company’s challenges in scaling its operations and capturing a larger market share. Factors such as intense competition from major players like Jio and Airtel, declining cable TV subscriptions, and slower-than-expected broadband expansion have likely contributed to this trend. Additionally, limited innovation and slower adoption of advanced technologies may have restricted the company’s ability to attract new customers and retain existing ones.

Overall, while the company has managed to maintain stable revenues without significant decline, the lack of robust growth indicates structural challenges in its business model. To improve its revenue trajectory, Hathway will need to focus on strengthening its broadband offerings, enhancing customer experience, and investing in infrastructure upgrades to remain competitive in the long term.

Profit Growth (CAGR%) Of Hathway

| Year | Net Profit (₹ Cr) |

|---|---|

| 2021 | 253 |

| 2022 | 130 |

| 2023 | 65 |

| 2024 | 99 |

| 2025 | 93 |

Profit trend is volatile, as clearly reflected in the above table. The company reported a strong net profit of ₹253 crore in 2021, but this figure declined significantly to ₹130 crore in 2022 and further dropped to ₹65 crore in 2023. This sharp decline indicates substantial pressure on the company’s margins and overall business performance during this period. Although there was a partial recovery in 2024 with profits rising to ₹99 crore, the improvement was not sustained, as profits slightly decreased again to ₹93 crore in 2025.

This inconsistent profit trajectory suggests that the company is facing operational challenges, including rising costs, competitive pricing pressures, and possibly declining revenues from its traditional cable TV segment. Additionally, the inability to maintain stable profitability highlights inefficiencies in cost management and limited scalability in its current business model. The modest recovery seen in recent years indicates some efforts toward stabilization, but it is not strong enough to signal a clear turnaround.

Overall, the fluctuating profit trend raises concerns about the company’s long-term earnings visibility. For sustained growth, Hathway needs to focus on improving operational efficiency, expanding its higher-margin broadband segment, and strengthening its competitive positioning in the market.

EPS & ROE Trends Of Hathway

| Year | EPS | ROE |

|---|---|---|

| 2021 | 1.43 | 4.61% |

| 2022 | 0.73 | 3.21% |

| 2023 | 0.37 | 1.57% |

| 2024 | 0.56 | 2.34% |

| 2025 | 0.52 | 2.13% |

ROE is very low across the observed period, remaining in the range of approximately 1.5% to 4.6%. Ideally, a healthy company should maintain a Return on Equity above 15%, which indicates efficient utilization of shareholders’ funds to generate profits. However, Hathway’s consistently low ROE reflects weak operational efficiency and limited profitability relative to its equity base.

From the table, it is evident that ROE has declined significantly from 4.61% in 2021 to as low as 1.57% in 2023, followed by only a marginal recovery to around 2.13% in 2025.

This downward trend aligns with the decline in net profits during the same period, indicating that the company has struggled to maintain earnings growth. The low ROE also suggests that the company is not effectively converting its investments into higher returns, which can be a concern for long-term investors.

Such performance may be attributed to increasing competition, pricing pressure, and limited scalability in its core business segments. Additionally, the modest improvement in recent years is not strong enough to signal a clear turnaround. Overall, the persistently low ROE highlights the need for strategic improvements in profitability and capital allocation to enhance shareholder value.

Debt-to-Equity Ratio Of Hathway

| Year | D/E Ratio |

|---|---|

| 2021 | 0.13 |

| 2022 | 0.12 |

| 2023 | 0.15 |

| 2024 | 0.15 |

| 2025 | 0.17 |

Debt levels for Hathway Cable & Datacom Ltd have remained consistently low over the years, as reflected in the debt-to-equity ratio ranging between 0.12 and 0.17 from 2021 to 2025. This indicates that the company relies minimally on external borrowings to fund its operations and growth, which is a strong positive from a financial risk perspective.

A low debt burden reduces interest obligations, thereby protecting profitability even during periods of revenue pressure or market volatility.

The gradual increase in the debt-to-equity ratio from 0.12 in 2022 to 0.17 in 2025 is still within a comfortable range and does not raise immediate concerns. Instead, it may suggest that the company is cautiously utilizing leverage to support its business activities without compromising financial stability. Maintaining such a balanced capital structure allows Hathway to remain resilient against economic uncertainties and industry challenges.

Overall, the company’s low leverage profile enhances its creditworthiness and provides flexibility for future investments, especially in upgrading broadband infrastructure and expanding digital services. This financial discipline is a key strength, particularly in a competitive sector where companies often take on significant debt to scale operations.

Net Profit Margins Of Hathway

| Year | Margin |

|---|---|

| 2021 | 14.6% |

| 2022 | 7.2% |

| 2023 | 3.5% |

| 2024 | 5.0% |

| 2025 | 4.6% |

Margins have declined significantly over the years, indicating sustained pressure on the company’s profitability. As seen in the table above, net profit margins dropped sharply from 14.6% in 2021 to 7.2% in 2022, and further declined to 3.5% in 2023.

Although there was a slight recovery to 5.0% in 2024, margins again slipped to 4.6% in 2025. This trend reflects increasing operational costs, competitive pricing pressures, and limited pricing power in the cable and broadband segment.

The decline in margins suggests that the company is struggling to maintain cost efficiency while sustaining revenue growth. Rising expenses related to network maintenance, customer acquisition, and service improvements may be impacting overall profitability. Additionally, intense competition from major players like Jio and Airtel is forcing the company to offer competitive pricing, which further compresses margins.

While the slight improvement in 2024 indicates some operational adjustments, the inconsistency in margin recovery highlights the need for a more structured approach to cost management. To improve profitability, the company must focus on optimizing operational efficiency, reducing unnecessary expenses, and enhancing service quality to retain customers. Strengthening its broadband segment and leveraging technology for automation can also help improve margins over the long term.

Market Capitalization Of Hathway

| Year | Market Cap (₹ Cr) |

|---|---|

| 2021 | ~5,000 |

| 2022 | ~3,500 |

| 2023 | ~2,500 |

| 2024 | ~2,000 |

| 2025 | ~1,742 |

Market capitalization has witnessed a consistent decline over the past few years, falling from approximately ₹5,000 crore in 2021 to around ₹1,742 crore in 2025. This sharp reduction reflects a sustained erosion in investor confidence and indicates that the market has been reassessing the company’s growth prospects and overall business performance. The downward trend aligns with the company’s weak financial indicators, including slow revenue growth, declining profitability, and low return on equity.

Additionally, the absence of strong growth triggers, such as expansion initiatives or significant improvements in operational efficiency, has further contributed to negative market sentiment. Increasing competition from major telecom and broadband players like Jio and Airtel has also impacted Hathway’s ability to retain and grow its customer base, thereby affecting its valuation.

The declining market cap suggests that investors are cautious about the company’s future outlook and are possibly shifting their investments toward companies with stronger growth potential and better financial performance. Unless Hathway demonstrates a clear turnaround through improved earnings, enhanced service quality, and strategic investments in broadband infrastructure, it may continue to face pressure on its market valuation in the coming years.

Dividend Yield Of Hathway

| Year | Dividend |

|---|---|

| 2021 | 0% |

| 2022 | 0% |

| 2023 | 0% |

| 2024 | 0% |

| 2025 | 0% |

The company does not pay dividends. Investors do not get regular income from this stock.

Conclusion

Hathway Cable & Datacom Ltd is a stable but slow growing company. It has strong promoter backing and low debt which are positive factors. But the company is facing major challenges like low growth, weak profitability and strong competition.

The stock is currently under pressure and showing weak trend. Long term growth depends on broadband expansion and service improvement. Investors should be careful. This stock is suitable only for high risk investors who believe in long term turnaround. Always do proper research before investing.

Related Posts :

Share This Post