MTNL Share Price Target 2026, 2027, 2028, 2029, 2030, 2035, 2040, 2050: Complete Analysis and Investment Outlook

MTNL Share Price Target

(MTNL) Mahanagar Telephone Nigam is a government-owned telecom company that provides fixed-line, broadband, and enterprise services in Mumbai and Delhi. Established in 1986, MTNL was once a dominant player in India’s telecom sector. However, over the past decade, the company has faced severe financial distress due to intense competition from private operators, declining landline usage, and failure to adapt to mobile and data-centric services.

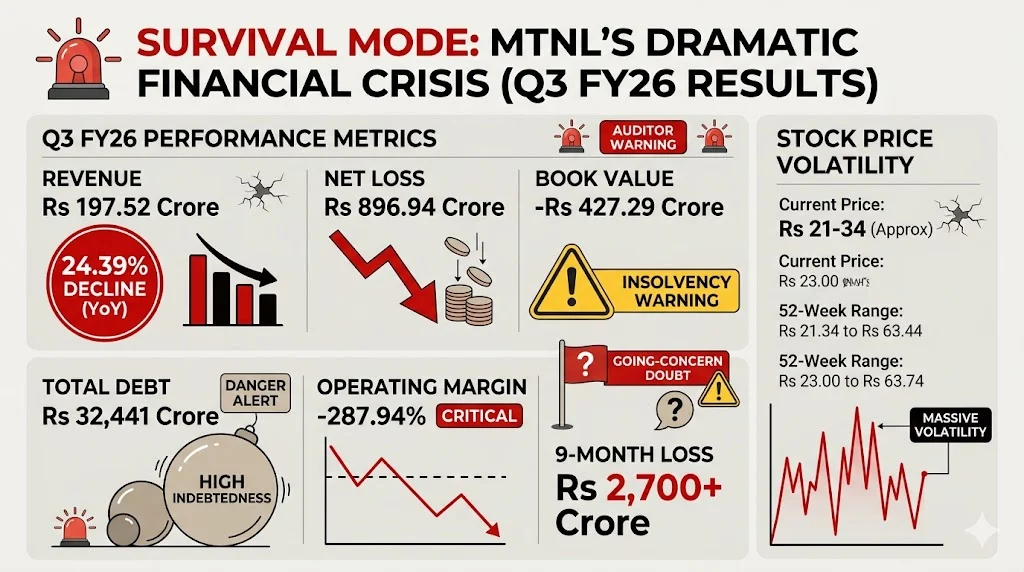

As of April 2026, MTNL trades at approximately Rs 21 to Rs 34 per share, with a market capitalization of around Rs 14.5 billion to Rs 28.12 billion. The stock has experienced extreme volatility, trading between a 52-week low of Rs 23.00 and a 52-week high of Rs 63.74. The company continues to report massive losses, with Q3 FY26 showing a net loss of Rs 896.94 crore and revenue declining 25.6% year-on-year.

This comprehensive analysis provides detailed share price targets for MTNL from 2026 through 2050, based on fundamental analysis, government support measures, asset monetization plans, and the potential BSNL integration. Investors should note that MTNL represents an extremely high-risk investment suitable only for speculators with strong risk tolerance.

Table of Contents

MTNL Current Financial Overview

Understanding the current financial position is essential before examining future price targets. The company remains in severe financial distress with deteriorating metrics.

| Financial Metric | Value (Q3 FY26) | Year-Ago Comparison | Trend Assessment |

|---|---|---|---|

| Revenue | Rs 197.52 crore | Down 24.39% YoY | Sharp decline |

| Operating Profit | -Rs 174.15 crore | Down 33.91% | Deteriorating |

| Net Loss | Rs 896.94 crore | Improved 7.28% YoY | Still massive |

| 9-Month FY26 Loss | Rs 2,700+ crore | Deep losses continue | Critical |

| Book Value Per Share | -Rs 427.29 | Negative net worth | Insolvency risk |

| Total Debt | Rs 324.41 billion | Rs 32,441 crore | Extreme leverage |

| Cash Position | Rs 2.1 billion | Rs 210 crore | Insufficient |

| Operating Margin | -287.94% | Deeply negative | Unsustainable |

| Revenue Per Share | Rs 9.20 | Declining | Weak fundamentals |

The company reported its Q3 FY26 results in February 2026, showing a 25.6% year-on-year revenue decline to Rs 197.52 crore. Net losses remained elevated at Rs 896.94 crore, though this represented a slight 7.28% improvement from the previous year. Auditors issued severe warnings about accounting anomalies and going-concern doubts.

MTNL has defaulted on loan repayments exceeding Rs 8,300 to 8,700 crore to multiple public sector banks including Union Bank, Bank of India, PNB, and SBI. The company has also failed to fund escrow accounts for interest payments on sovereign guarantee-backed bonds, citing insufficient funds.

Key Factors Influencing MTNL Share Price

Multiple factors will determine whether MTNL achieves any of its price targets in the coming years. Understanding these drivers helps investors assess the probability of success.

Government Support and BSNL Integration

The Indian government remains committed to supporting MTNL through various revival measures. From January 1, 2025, BSNL has taken over day-to-day telecom operations in Delhi and Mumbai under a service agreement. BSNL handles CAPEX and OPEX with an aim for EBITDA-neutral operations for MTNL.

The government has formed a committee to explore long-term restructuring options, including a potential full merger or subsidiary structure. The Department of Telecommunications has clarified that there are no plans to shut down MTNL, and proceeds from asset monetization are being used in accordance with Cabinet approvals.

The government has provided multiple revival packages over the years, with cumulative support exceeding Rs 3.2 lakh crore for the BSNL/MTNL ecosystem. However, Budget 2026 showed a 35% cut in DoT allocation, raising concerns about reduced capital support.

Asset Monetization Strategy

MTNL is actively selling land and properties to ease financial stress. Key recent developments include:

- December 2025: Board approval for sale of residential housing block in Mumbai’s BKC to NABARD for Rs 350.72 crore

- Property details: GN Block, BKC Quarters, 28 residential quarters, 2,680 square meters plot area, 4,019 square meters built-up area

- FY26 target: Rs 4,573 crore from MTNL asset monetization

- BSNL and MTNL together aim to monetize Rs 1,000+ crore in land assets in FY26

- Additional property leasing agreements signed (e.g., Rs 68.43 crore in Bihar)

The asset monetization is being conducted under DIPAM guidelines with Presidential Approval granted on July 17, 2020. However, state-level hurdles may delay timelines.

Operational Handover to BSNL

Since January 1, 2025, BSNL has taken over MTNL’s operations in Delhi and Mumbai. This arrangement aims to:

- Improve operational efficiency through centralized management

- Reduce costs through shared infrastructure

- Achieve EBITDA-neutral operations for MTNL

- Provide a pathway to potential full merger

The long-term vision includes MTNL potentially becoming a subsidiary of BSNL or full integration into the BSNL structure.

Competitive Position

MTNL faces existential competitive threats:

- Reliance Jio: 506.4 million subscribers, aggressive pricing, 5G leadership

- Bharti Airtel: 364.2 million subscribers, premium positioning, industry-leading ARPU of Rs 259

- Vodafone Idea: 193 to 205 million subscribers, recovering with government support

- BSNL: Returning to profitability with Rs 280 crore net profit in Q4 FY25

MTNL lacks presence in modern telecom services. The company has minimal mobile market share, no 4G/5G infrastructure of its own, and relies on BSNL for network services. Subscriber base continues to shrink as customers migrate to private operators.

MTNL Share Price Target 2026

The year 2026 represents a survival phase for MTNL. The stock will remain highly volatile, reacting to news on asset sales, government decisions, and quarterly results.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 28 | Rs 38 | Asset sale approvals, Q3 FY26 results |

| February | Rs 30 | Rs 40 | BKC property sale completion |

| March | Rs 25 | Rs 35 | Q4 FY26 results preview, FY27 planning |

| April | Rs 22 | Rs 32 | Q4 FY26 results, annual loss figures |

| May | Rs 24 | Rs 36 | Monsoon season, operational updates |

| June | Rs 26 | Rs 42 | Asset monetization progress |

| July | Rs 28 | Rs 45 | Government policy announcements |

| August | Rs 30 | Rs 48 | Q1 FY27 results, BSNL integration updates |

| September | Rs 32 | Rs 50 | Festive season, property sale news |

| October | Rs 28 | Rs 44 | Q2 FY27 results, quarterly losses |

| November | Rs 26 | Rs 40 | Annual planning, FY28 outlook |

| December | Rs 24 | Rs 38 | Year-end positioning, 2027 target revisions |

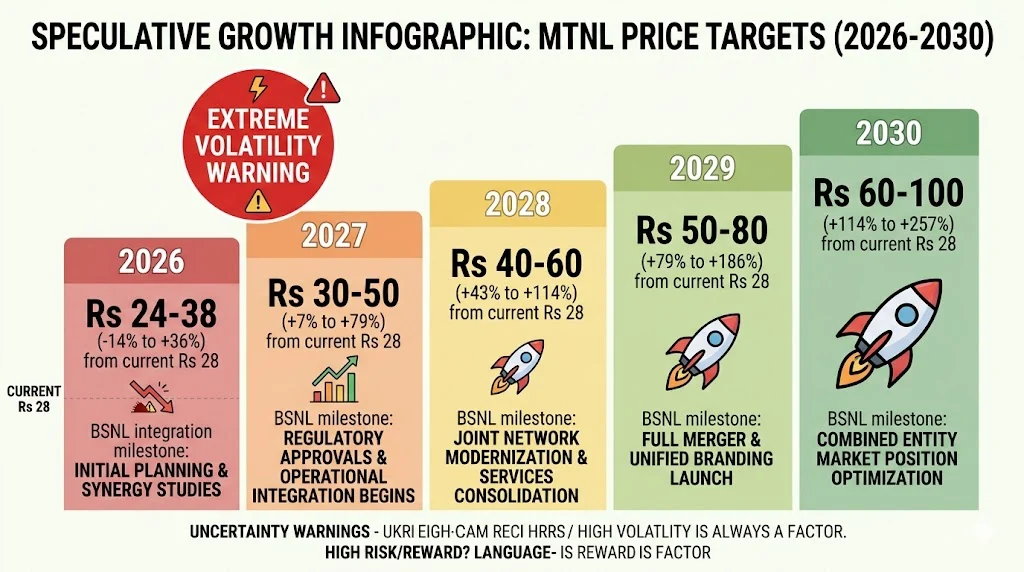

2026 Year-End Target: Rs 24 to Rs 38

The 2026 price target range represents potential upside of 0% to 58% from current levels of Rs 24 to Rs 34. This wide range reflects extreme uncertainty. The target assumes successful execution of asset monetization plans and continued government support.

Key risks to the 2026 target include:

- Failure to complete planned asset sales

- Further deterioration in financial results

- Government policy changes reducing support

- Complete operational shutdown

- Delisting due to prolonged financial distress

MTNL Share Price Target 2027

By 2027, MTNL’s future will depend heavily on government action and the progress of BSNL integration.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 26 | Rs 42 | FY27 annual results, government decisions |

| February | Rs 28 | Rs 45 | Full-year FY27 results, auditor comments |

| March | Rs 30 | Rs 48 | Q4 FY27 close, FY28 planning |

| April | Rs 32 | Rs 50 | Q1 FY28 results, summer season |

| May | Rs 35 | Rs 55 | Asset monetization completion |

| June | Rs 32 | Rs 50 | Monsoon impact, operational review |

| July | Rs 34 | Rs 58 | Government policy updates |

| August | Rs 36 | Rs 62 | Q2 FY28 results, integration progress |

| September | Rs 38 | Rs 65 | Festive season, property sales |

| October | Rs 35 | Rs 58 | Q3 FY28 results, loss trends |

| November | Rs 32 | Rs 52 | Annual guidance, long-term outlook |

| December | Rs 30 | Rs 50 | Year-end targets, 2028 outlook |

2027 Year-End Target: Rs 30 to Rs 50

The 2027 target range reflects expectations that government support continues and asset monetization provides liquidity. By this point:

- Major asset sales should be completed

- BSNL integration should show tangible progress

- Operational costs should reduce through shared services

- Revenue decline should stabilize

However, the company will likely remain loss-making with negative net worth. The stock will continue to trade based on speculative interest rather than fundamentals.

MTNL Share Price Target 2028

By 2028, MTNL may see some improvement if restructuring plans are executed properly.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 35 | Rs 55 | FY28 annual results, three-year review |

| February | Rs 38 | Rs 58 | Full-year FY28 results, profitability timeline |

| March | Rs 40 | Rs 60 | Q4 FY28 close, FY29 guidance |

| April | Rs 42 | Rs 62 | Q1 FY29 results, operational metrics |

| May | Rs 45 | Rs 65 | BSNL integration milestones |

| June | Rs 42 | Rs 60 | Monsoon season, network performance |

| July | Rs 44 | Rs 68 | Government policy decisions |

| August | Rs 46 | Rs 70 | Q2 FY29 results, cost savings |

| September | Rs 48 | Rs 72 | Festive demand, digital services |

| October | Rs 45 | Rs 68 | Q3 FY29 results, financial health |

| November | Rs 42 | Rs 62 | Annual planning, 2030 vision |

| December | Rs 40 | Rs 60 | Year-end targets, long-term outlook |

2028 Year-End Target: Rs 40 to Rs 60

The 2028 target assumes MTNL benefits from reduced debt burden and improved operations under BSNL management. The telecom sector in India continues growing due to increasing data usage. However, MTNL needs meaningful infrastructure investment to benefit from this trend.

Government support remains essential. Policies aimed at supporting PSU telecom companies can help MTNL survive. Long-term growth requires strong execution of revival plans.

MTNL Share Price Target 2029

By 2029, MTNL’s performance will depend on how well it adapts to the changing telecom environment.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 45 | Rs 70 | FY29 annual results, turnaround review |

| February | Rs 48 | Rs 75 | Full-year FY29 results, path to stability |

| March | Rs 50 | Rs 80 | Q4 FY29 close, FY30 planning |

| April | Rs 52 | Rs 82 | Q1 FY30 results, operational stability |

| May | Rs 55 | Rs 85 | BSNL merger finalization |

| June | Rs 52 | Rs 80 | Monsoon impact, service continuity |

| July | Rs 54 | Rs 88 | Government support confirmation |

| August | Rs 56 | Rs 90 | Q2 FY30 results, financial improvements |

| September | Rs 58 | Rs 92 | Festive season, revenue growth |

| October | Rs 55 | Rs 88 | Q3 FY30 results, loss reduction |

| November | Rs 52 | Rs 82 | Annual guidance, 2030 targets |

| December | Rs 50 | Rs 80 | Year-end positioning, decade outlook |

2029 Year-End Target: Rs 50 to Rs 80

By 2029, MTNL may achieve some financial stability if restructuring is successful. Asset monetization and cost control can support this stability. However, competition from private players remains intense. The company needs to improve service quality to retain any remaining customers.

Investors should consider the risks carefully. MTNL is not a typical growth stock. It represents a turnaround story with extremely high uncertainty.

MTNL Share Price Target 2030

By 2030, MTNL may achieve stability if the decade-long restructuring effort succeeds.

| Month | Minimum Price Target | Maximum Price Target | Key Catalysts |

|---|---|---|---|

| January | Rs 55 | Rs 85 | FY30 annual results, decade achievement |

| February | Rs 58 | Rs 90 | Full-year FY30 results, milestone review |

| March | Rs 60 | Rs 95 | Q4 FY30 close, FY31 planning |

| April | Rs 62 | Rs 98 | Q1 FY31 results, sustained operations |

| May | Rs 65 | Rs 100 | BSNL full integration |

| June | Rs 62 | Rs 95 | Operational review, cost efficiency |

| July | Rs 64 | Rs 105 | Government policy support |

| August | Rs 66 | Rs 110 | Q2 FY31 results, financial health |

| September | Rs 68 | Rs 115 | Festive season, revenue growth |

| October | Rs 65 | Rs 108 | Q3 FY31 results, profitability path |

| November | Rs 62 | Rs 102 | Annual planning, 2035 vision |

| December | Rs 60 | Rs 100 | Year-end targets, long-term outlook |

2030 Year-End Target: Rs 60 to Rs 100

By 2030, MTNL may achieve operational stability if restructuring is successful. The company can benefit from telecom sector growth. Integration with BSNL can create a stronger PSU telecom entity.

However, achieving this scenario requires major improvements. The company needs to modernize its network and improve customer experience. Without these changes, growth remains limited.

Long-term investors should monitor execution of revival plans. The success of these plans will determine future growth.

MTNL Share Price Target 2035

Looking further ahead to 2035, MTNL’s success will depend on maintaining relevance in a rapidly evolving telecom landscape.

| Scenario | Minimum Price Target | Maximum Price Target | Probability Assessment |

|---|---|---|---|

| Bull Case | Rs 100 | Rs 150 | 20% probability |

| Base Case | Rs 80 | Rs 120 | 40% probability |

| Bear Case | Rs 40 | Rs 60 | 40% probability |

2035 Target: Rs 80 to Rs 120

By 2035, the telecom sector will be driven by advanced technologies. MTNL’s ability to invest in these technologies while maintaining operations will determine its long-term position. The company must avoid falling further behind private competitors in technology leadership.

MTNL Share Price Target 2040

By 2040, MTNL could be a stable telecom player if it successfully navigates the challenges of the 2020s and 2030s.

| Scenario | Minimum Price Target | Maximum Price Target | Key Drivers |

|---|---|---|---|

| Bull Case | Rs 150 | Rs 200 | Market leadership, innovation |

| Base Case | Rs 100 | Rs 150 | Stable operations, steady growth |

| Bear Case | Rs 50 | Rs 80 | Continued marginalization |

2040 Target: Rs 100 to Rs 150

The 2040 target range reflects significant uncertainty over such long time horizons. Key variables include:

- Evolution of telecom technology beyond 5G/6G

- Regulatory environment and spectrum policy

- Competitive dynamics with potential new entrants

- MTNL’s ability to maintain technology parity

- Success of BSNL integration and combined operations

MTNL Share Price Target 2050

Projecting to 2050 involves substantial speculation, but provides a framework for long-term thinking.

| Scenario | Minimum Price Target | Maximum Price Target | Long-Term Vision |

|---|---|---|---|

| Bull Case | Rs 200 | Rs 300 | Industry leader, global expansion |

| Base Case | Rs 150 | Rs 250 | Stable Indian operator, solid returns |

| Bear Case | Rs 80 | Rs 150 | Marginal player, limited growth |

2050 Target: Rs 150 to Rs 250

By 2050, MTNL could be a completely transformed entity, potentially:

- Fully integrated into BSNL or successor organization

- Provider of specialized government and enterprise services

- Significant infrastructure assets in prime urban locations

- Mature dividend-paying stock with stable returns (if turnaround succeeds)

Investment Analysis: Is MTNL a Good Buy?

Bull Case Arguments

- Government ownership provides backing and prevents complete collapse

- Asset monetization opportunities in prime Mumbai and Delhi real estate

- Potential BSNL integration creating operational synergies

- Low stock price offering significant upside potential if turnaround succeeds

- Spectrum assets worth monetizing

- Possible turnaround if restructuring plans work effectively

- BSNL’s return to profitability (Rs 280 crore in Q4 FY25) provides template

Bear Case Arguments

- Persistent financial losses with deepening revenue decline (25.6% YoY in Q3 FY26)

- Massive debt of Rs 32,441 crore with ongoing defaults

- Negative net worth of Rs 427.29 per share indicating insolvency

- Outdated infrastructure with no 4G/5G network of its own

- Intense competition from Jio, Airtel, and recovering Vodafone Idea

- Uncertain execution and success of revival plans

- Auditor warnings about going-concern status

- TRAI penalties for poor Quality of Service

- Risk of delisting or forced restructuring

- No dividend payments for over 15 years

Shareholding Pattern

Understanding who owns MTNL provides insight into market confidence levels.

| Shareholder Category | Holding Percentage | Trend | Implication |

|---|---|---|---|

| Government (Promoter) | 56.25% | Stable | Majority control, strategic interest |

| Foreign Institutional Investors | 13.15% | Low | Limited foreign confidence |

| Retail and Other Investors | 30.6% | High speculation | Retail-driven volatility |

| Total Shares Outstanding | 630 million | Fixed | No recent dilution |

The government maintains majority control at 56.25%, providing stability but also raising questions about long-term strategy. Retail investor participation drives significant volatility with low free float.

Analyst Ratings and Market Sentiment

Brokerage houses and market analysts maintain overwhelmingly negative views on MTNL.

| Source | Rating/View | Key Concern |

|---|---|---|

| MarketsMojo | Strong Sell | Technical deterioration, flat financials, negative net worth |

| Auditor Reports | Severe Warning | Accounting anomalies, going-concern doubts |

| Retail Sentiment | Bearish | Poor service history, financial bonfire perception |

| Technical Analysis | Sell | Stock below all moving averages, bearish momentum |

Wallet Investor provides a contrarian AI-based forecast, suggesting the stock could reach Rs 69.37 by 2031, representing 101.82% upside over 5 years. However, this forecast appears optimistic given fundamental challenges.

Key Monitorables for Investors

Investors considering MTNL should track these metrics closely:

Financial Health

- Quarterly revenue trends (currently declining 25% YoY)

- Net loss trajectory (Rs 896 crore in Q3 FY26)

- Debt levels and default status

- Cash position and liquidity

- Book value (currently negative Rs 427)

Operational Metrics

- Subscriber base trends (continuing decline)

- Service quality metrics

- Network performance vs competitors

- BSNL integration progress

Asset Monetization

- Property sale completions

- Target achievement vs Rs 4,573 crore FY26 goal

- New asset sale announcements

- Government approval timelines

Government Policy

- BSNL merger timeline

- Revival package announcements

- DoT budget allocations

- Policy support for PSU telecom

Conclusion: Should You Buy MTNL?

MTNL represents one of the highest-risk investments in the Indian stock market. The company is effectively in survival mode with massive losses, negative net worth, and ongoing debt defaults.

Suitable for:

- Extreme risk speculators seeking lottery-ticket returns

- Traders capitalizing on volatility and news-based spikes

- Those with strong conviction in government bailout

- Investors with money they can afford to lose completely

Not suitable for:

- Conservative investors seeking stable returns

- Long-term wealth builders

- Dividend income seekers

- Risk-averse portfolios

- Investors requiring liquidity

The share price targets presented in this analysis range from Rs 24-38 for 2026 to Rs 60-100 for 2030, with long-term targets of Rs 100-150 by 2040. These represent potential returns of 0% to 300% from current levels, but come with substantial risk of 100% capital loss if the company fails or delists.

MTNL is not a typical investment. It is a speculation on government support, asset values, and potential turnaround. Most financial analysts recommend avoiding this stock entirely. Those who choose to invest should allocate only minimal capital and be prepared for complete loss.

Always conduct thorough due diligence, consult with financial advisors, and invest only what you can afford to lose. Past performance and price targets are not guarantees of future results.

Related Posts :

Share This Post