[Long Term] Tech & Telecom Stocks In India For Future Investment

![[Long Term] Tech & Telecom Stocks In India For Future Investment](https://personalloaneligibilitycalculator.in/wp-content/uploads/Long-Term-Tech-Telecom-Stocks-In-India-For-Future-Investment.webp)

[Long Term] Tech & Telecom Stocks In India For Future Investment

If you are searching for the best tech and telecom stocks in India for long term investment, then you are thinking in the right direction. This sector is not just growing. It is transforming very fast. Many investors look at popular stocks like TCS, Infosys, and Airtel. These are strong companies. But they are already well covered everywhere.

The real opportunity lies deeper. It lies in companies that are connected to BharatNet, 5G expansion, AI adoption, and Digital India infrastructure. These companies are not yet fully discovered by retail investors. That is why they offer higher upside potential by 2030.

Most articles you read online focus only on safe options. They miss high growth mid cap and turnaround stories. They do not talk about real catalysts like new government orders or telecom recovery trends. That creates a gap. This blog fills that gap. In this article, you will understand both safe and high growth stocks. You will also see realistic 2030 targets, risks, and strategy. This will help you build a strong long term portfolio.

Table of Contents

Key Takeaways On Tech & Telecom Stocks

- Tech and telecom sectors will grow strongly till 2030 due to AI and 5G

- High growth mid cap stocks offer better upside but carry higher risk

- BharatNet and Digital India projects are major future catalysts

- Turnaround companies can give big returns but need patience

- Smart investors combine stable stocks with high potential bets

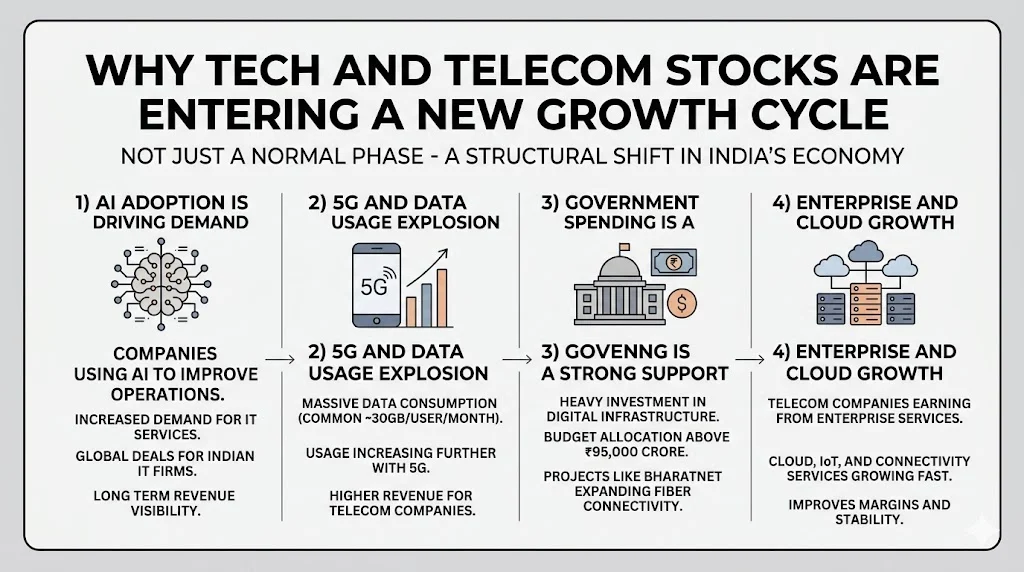

Why Tech And Telecom Stocks Are Entering A New Growth Cycle

This is not just a normal growth phase. It is a structural shift in India’s economy. India is moving towards a digital first ecosystem. Every sector depends on data, connectivity, and automation. That is why both IT and telecom sectors are growing together.

1) AI Adoption Is Driving Demand

Companies are now using AI to improve operations. This is increasing demand for IT services. Indian IT firms are getting global deals. This creates long term revenue visibility.

2) 5G And Data Usage Explosion

India already has massive data consumption. Around 30GB per user per month is common now. With 5G, usage will increase further. This means higher revenue for telecom companies.

3) Government Spending Is A Strong Support

Government is investing heavily in digital infrastructure. Budget allocation above ₹95,000 crore shows long term commitment. Projects like BharatNet are expanding fiber connectivity across India.

4) Enterprise And Cloud Growth

Telecom companies are earning from enterprise services now. Cloud, IoT, and connectivity services are growing fast. This improves margins and stability.

Large Cap Stocks That Provide Stability

Before going into high growth names, you must understand stable options. These companies provide safety and consistent returns.

| Name | Info | Low | Medium |

|---|---|---|

| TCS | Strong cash flow and AI deals | Low |

| Infosys | Global growth and AI platforms | Low |

| Bharti Airtel | Strong telecom position | Medium |

| HCL Tech | Cloud and cybersecurity focus | Low |

These companies may not give 10x returns. But they provide steady compounding. They are important for portfolio balance.

Growth Opportunity Stocks With Strong Potential

These companies are slightly aggressive. They are growing faster than large caps.

- Tech Mahindra works in telecom and IT both

- Reliance benefits from Jio, broadband, and data centers

- LTIMindtree is winning large deals globally

- Persistent Systems is strong in AI and analytics

These companies can outperform large caps in the long run. But they still carry moderate risk.

High Upside Tech & Telecom Stocks For 2030 (Deep Dive)

This is the most important section. These are the stocks that most investors are searching right now. These are high risk but high reward opportunities.

Vodafone Idea: The Turnaround Bet

Vodafone Idea is one of the most discussed telecom stocks in India, mainly because it represents a classic high-risk turnaround story. The company has been under financial stress for years, but recent developments show early signs of stabilization.

As of March 2026, the stock trades in the ₹9 to ₹11 range, with a market capitalization of around ₹70,000–₹75,000 crore. The company’s Average Revenue Per User (ARPU) has improved from ₹135 in FY23 to around ₹160–₹170, driven by tariff hikes. Management has guided for ARPU to cross ₹200 in the coming years, which is critical for profitability.

On the fundamentals side, Vodafone Idea still carries a very high debt burden of over ₹2 lakh crore, including AGR dues and spectrum liabilities. However, a major positive is government support, where a significant portion of dues has been converted into equity, making the government one of the largest shareholders. This reduces immediate cash pressure and improves survival chances.

The company’s key moat lies in its existing subscriber base of over 200 million users and its pan-India spectrum holdings. If it successfully executes its 4G expansion and planned 5G rollout, it can retain and grow its user base. Additionally, the telecom industry in India is effectively a three-player market, which increases the importance of Vodafone Idea’s survival.

However, profitability remains a challenge. The company is still reporting losses, and network investment is required to compete with Jio and Airtel. Any delay in fundraising or capex execution can impact growth.

The 2030 target range of ₹40 to ₹90 assumes successful turnaround, ARPU growth, and improved margins. This stock is suitable only for aggressive investors who understand the risks and can hold for the long term.

MTNL: High Risk PSU Revival Story

MTNL (Mahanagar Telephone Nigam Limited) is a government-owned telecom PSU that operates mainly in Delhi and Mumbai. Over the years, the company has faced severe financial stress due to intense competition from private players like Jio and Airtel. As of recent financial data, MTNL has reported continuous losses, with annual losses exceeding ₹3,000–₹4,000 crore and a negative net worth. The company also carries a very high debt burden, estimated above ₹20,000 crore, which remains one of its biggest challenges.

However, the key support for MTNL comes from the Government of India. The government has already provided financial relief packages, including sovereign guarantees for bonds and asset monetization plans. MTNL also owns valuable real estate assets in prime locations of Delhi and Mumbai, which can be monetized to improve its balance sheet. This asset base acts as a hidden value and provides some downside protection.

In terms of business moat, MTNL’s primary advantage is its legacy infrastructure, fiber network, and strong presence in government contracts. It also benefits from potential collaboration with BSNL for 4G and future 5G rollout, which could revive its operational relevance. If the government successfully executes telecom PSU revival plans, MTNL could see improved revenue streams.

From a valuation perspective, the stock trades more on speculation than fundamentals. Revenue growth remains weak, and profitability is still negative. However, any positive policy announcement or revival plan can trigger sharp price movements.

The 2030 price target is estimated around ₹200 to ₹250 in highly optimistic scenarios, assuming successful turnaround and debt restructuring. This stock remains extremely high risk and is suitable only for very small allocation in a diversified portfolio.

HFCL: Strong BharatNet And Fiber Play

HFCL is a key player in India’s telecom infrastructure ecosystem, especially in optical fiber cables (OFC), telecom equipment, and network solutions. The company has built a strong position in fiber manufacturing, with an installed capacity of over 30 million fiber kilometers annually, making it one of the leading domestic suppliers.

From a financial perspective, HFCL has shown steady growth. In FY25, the company reported revenue of around ₹4,500–₹5,000 crore with EBITDA margins in the range of 14–16%. Net profit has been improving consistently, supported by better order execution and higher-margin product mix. The order book remains strong at over ₹7,000 crore, providing clear revenue visibility for the next 2–3 years.

One of HFCL’s biggest moats is its deep integration with government-led projects like BharatNet Phase 3, where it has secured large-scale contracts for fiber deployment and networking equipment. This gives the company a strong advantage over smaller competitors. Additionally, HFCL is investing in next-generation technologies like 5G radio equipment, Wi-Fi 6 solutions, and defense communication systems, which can drive future growth.

The company also benefits from the “Make in India” push, as telecom operators prefer domestic suppliers to reduce dependency on imports. Its backward integration in fiber manufacturing helps maintain cost efficiency and margins.

However, risks remain. HFCL is still dependent on government orders, and any delay in project execution can impact cash flows. Working capital requirements are also relatively high. Considering its strong order book, improving financials, and exposure to long-term telecom infrastructure growth, HFCL has the potential to reach ₹223 to ₹500 or higher by 2030 in bullish scenarios.

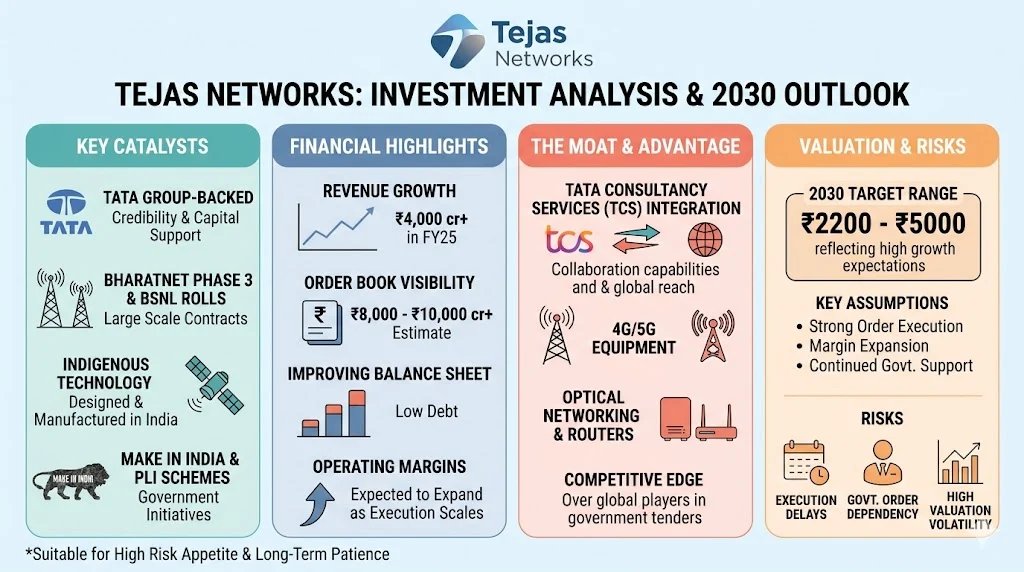

Tejas Networks: The Star Performer

Tejas Networks is gaining strong attention due to its strategic positioning in India’s telecom equipment ecosystem and its recent large-scale BharatNet Phase 3 contracts. The company is a Tata Group-backed telecom gear manufacturer, which gives it a strong credibility advantage and access to capital support.

From a financial perspective, Tejas has shown a sharp turnaround. Revenue has grown significantly, crossing ₹4,000 crore in FY25, compared to under ₹1,000 crore just a few years ago. Order book visibility is strong, estimated above ₹8,000–₹10,000 crore, largely driven by government and telecom operator contracts. The company has also improved its balance sheet, with relatively low debt and improving operating margins, which are expected to expand as execution scales.

Its core moat lies in indigenous telecom technology development. Tejas designs and manufactures optical networking products, routers, and 4G/5G equipment in India, aligning perfectly with the government’s “Make in India” and PLI schemes. This gives it a competitive edge over global players in government tenders. Additionally, its integration with Tata Consultancy Services and Tata Sons ecosystem strengthens its execution capabilities and global reach.

The company is actively deploying thousands of routers under BharatNet and is also participating in BSNL’s 4G rollout, which is a multi-year opportunity. If execution remains strong, revenue and profit growth can compound at a high rate.

At a current price of around ₹331 (March 2026), the stock trades at a premium valuation, reflecting high growth expectations. The 2030 target range of ₹2200 to ₹5000 assumes strong order execution, margin expansion, and continued government support. However, risks remain. Execution delays, dependency on government orders, and high valuation multiples can lead to volatility. This stock is suitable for investors with high risk appetite and long-term patience.

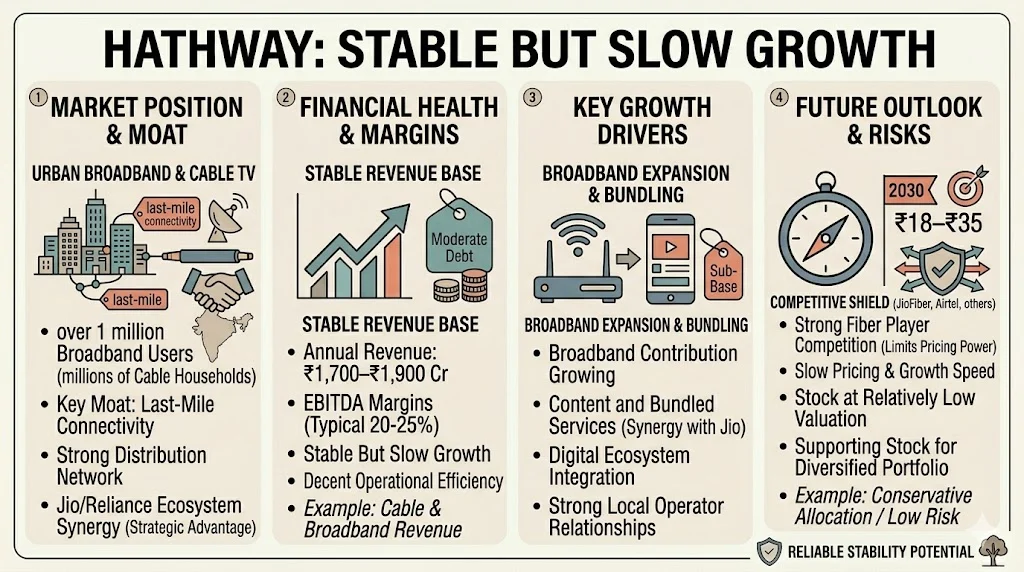

Hathway: Stable But Slow Growth

Hathway Cable & Datacom is a broadband and cable TV service provider, primarily focused on urban and semi-urban markets. The company operates under the Reliance Industries ecosystem, which gives it a strategic advantage in terms of network expansion, content distribution, and long-term capital support.

From a fundamentals perspective, Hathway has shown stable but slow growth. The company’s revenue is in the range of ₹1,700–₹1,900 crore annually, with broadband contributing a growing share compared to traditional cable services. EBITDA margins are typically around 20–25%, indicating decent operational efficiency, but net profit margins remain low due to high depreciation and infrastructure costs.

The company has a subscriber base of over 1 million broadband users and millions of cable TV households, giving it a strong distribution network. Its key moat lies in last-mile connectivity and local cable operator relationships, which are difficult for new entrants to replicate quickly. Additionally, integration with Jio’s digital ecosystem can unlock future synergies in content and bundled services.

However, Hathway faces strong competition from JioFiber, Airtel Xstream, and other fiber players, which limits its pricing power and growth speed. Debt levels are moderate, and cash flows are stable but not aggressively expanding.

At a current price of around ₹9 to ₹10, the stock trades at a relatively low valuation compared to high-growth tech peers, reflecting its slow growth profile. By 2030, a realistic target range could be ₹18 to ₹35, assuming steady broadband expansion and improved margins.

Overall, Hathway is not a high-growth multibagger but a stable, low-risk supporting stock suitable for conservative allocation in a diversified telecom portfolio.

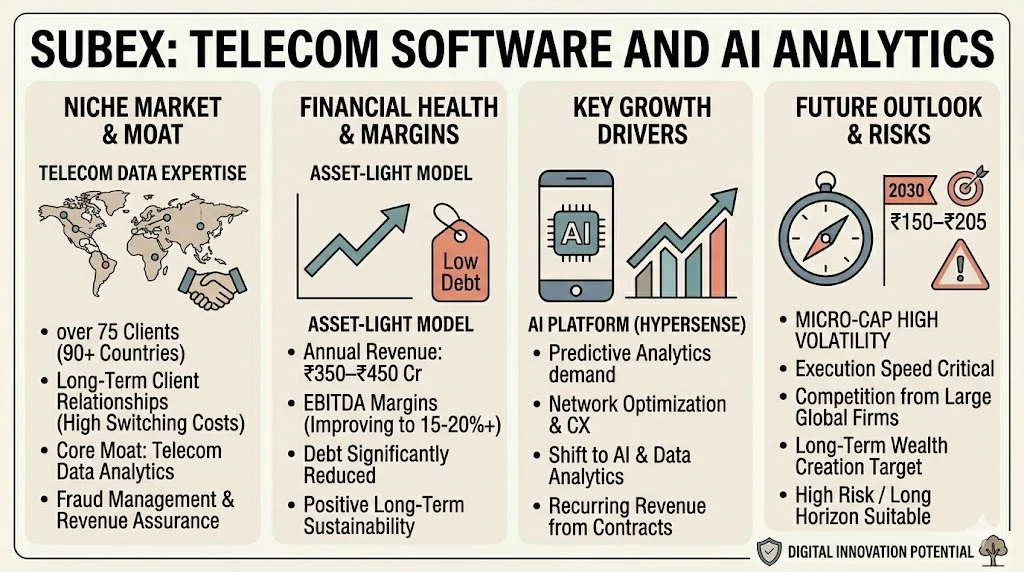

Subex: Telecom Software And AI Analytics

Subex is a niche telecom analytics company specializing in revenue assurance, fraud management, and network analytics solutions for global telecom operators. The company serves over 75 telecom clients across 90+ countries, which gives it a strong international presence despite its small size. Its core moat lies in deep domain expertise in telecom data analytics and long-term client relationships, as switching costs for telecom operators are relatively high once systems are integrated.

Financially, Subex has shown signs of improvement in recent years. The company operates with a relatively asset-light model and has been working towards improving margins through its AI-based platform, HyperSense. Revenue has been in the range of ₹350–₹450 crore annually, with EBITDA margins gradually improving towards 15–20% in better quarters. The company has also reduced debt significantly, which is a positive sign for long-term sustainability.

The shift towards AI and data analytics is a key growth driver. Telecom operators are increasingly relying on predictive analytics to reduce fraud, optimize networks, and improve customer experience. Subex’s investment in AI platforms positions it well to capture this demand. Additionally, recurring revenue from long-term contracts provides some stability to its business model.

At a current price of around ₹8, the stock is still considered a micro-cap with high volatility. The 2030 target range of ₹150 to ₹205 assumes strong execution, consistent revenue growth, and successful scaling of its AI offerings. However, risks remain high. The company faces competition from larger global analytics firms, and execution delays or client losses can impact performance. This stock is suitable only for high-risk investors with a long-term horizon.

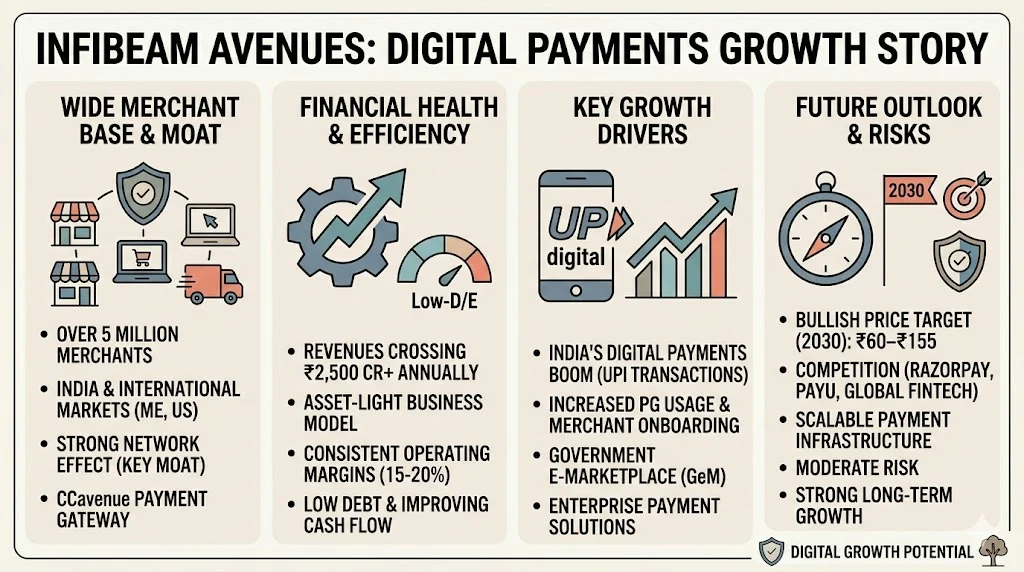

Infibeam Avenues: Digital Payments Growth Story

Infibeam Avenues is a digital payments and e-commerce infrastructure company that operates through its flagship payment gateway brand CCAvenue. The company processes millions of transactions daily and serves over 5 million merchants across India and international markets like the Middle East and the US. This wide merchant base creates a strong network effect, which acts as a key moat for the business.

From a financial perspective, Infibeam has shown steady revenue growth, with annual revenues crossing ₹2,500 crore in recent years. The company maintains a relatively asset-light model, which helps in generating consistent operating margins in the range of 15% to 20%. Its debt levels are low, and cash flow generation has been improving, which is a positive sign for long-term sustainability.

One of the biggest growth drivers is India’s digital payments boom. UPI transactions have crossed billions per month, and although Infibeam is not a direct UPI player, it benefits from the overall increase in online transactions, payment gateway usage, and merchant onboarding. Additionally, its expansion into government e-marketplace (GeM) services and enterprise payment solutions adds new revenue streams.

The company also has a technological moat through its scalable payment infrastructure, fraud detection systems, and multi-currency support, which makes it attractive for global merchants.

Looking ahead, if the company continues to grow its merchant base and improve margins, the 2030 price target of ₹60 to ₹155 appears achievable in a bullish scenario. However, competition from players like Razorpay, PayU, and global fintech firms remains a key risk. Overall, the stock offers moderate risk with strong long-term digital growth potential.

OnMobile Global: Niche Telecom Services

OnMobile Global is a niche telecom VAS (Value Added Services) and mobile entertainment company with a presence in over 60 countries. The company focuses on services like ringback tones, gaming, and digital engagement platforms for telecom operators. As of FY25, OnMobile reported revenue of around ₹600–650 crore with EBITDA margins in the range of 18–22%, showing improving operational efficiency.

One of the key strengths of OnMobile is its long-standing relationships with global telecom operators such as Vodafone, MTN, and Airtel. This creates a strong entry barrier (moat) because telecom integrations are complex and sticky in nature. Once deployed, these services tend to generate recurring revenue, which provides stability to the business model.

The company is also investing in AI-driven personalization and gaming platforms, which can act as future growth drivers. Its ONMO gaming platform is gaining traction, especially in international markets, and could significantly improve revenue mix over the next few years.

From a financial perspective, OnMobile has relatively low debt and maintains a healthy balance sheet, which reduces financial risk compared to many small-cap peers. However, growth has been inconsistent in the past, and revenue concentration in telecom clients remains a concern.

Current price is around ₹80–₹90 range (2026), and if the company successfully scales its gaming and digital platforms, 2030 targets are estimated between ₹445 to ₹660 in bullish scenarios. This implies a potential 5x–7x return, but execution will be critical. Overall, OnMobile is a high-risk, high-reward stock with a niche moat, global exposure, and improving fundamentals, but it requires patience and close monitoring.

Vishesh Infotecnics: Ultra High Risk Penny Stock

Vishesh Infotecnics is a micro-cap IT services and solutions company operating in niche areas like software development, IT consulting, and digital services. Being a penny stock, its market capitalization is extremely small, generally below ₹100 crore, which makes it highly volatile and sensitive to even minor changes in business performance.

Current price is around ₹0.33, reflecting low investor confidence and limited institutional participation. The company’s financials are weak compared to established IT firms. Revenue growth has been inconsistent over the years, and profitability remains either very low or negative in some periods. Return ratios like ROE and ROCE are also weak, indicating inefficient capital utilization. Debt levels are relatively low, but that is mainly due to the small scale of operations rather than strong financial discipline.

One of the few positives is that the company operates in the IT sector, which has long-term growth potential due to digital transformation, cloud adoption, and AI demand. However, Vishesh Infotecnics lacks a strong competitive moat. It does not have proprietary technology, large enterprise clients, or a strong brand presence. This makes it difficult to compete with mid and large IT companies.

2030 targets vary widely from ₹1.4 to ₹7 or more in extreme scenarios. Such projections are purely speculative and depend on a major turnaround in revenue growth, profitability, and business expansion.

This stock is suitable only for very small allocation, ideally less than 1–2% of your portfolio. Risk is extremely high due to low liquidity, weak fundamentals, and high price volatility. Investors should treat it as a speculative bet rather than a core investment.

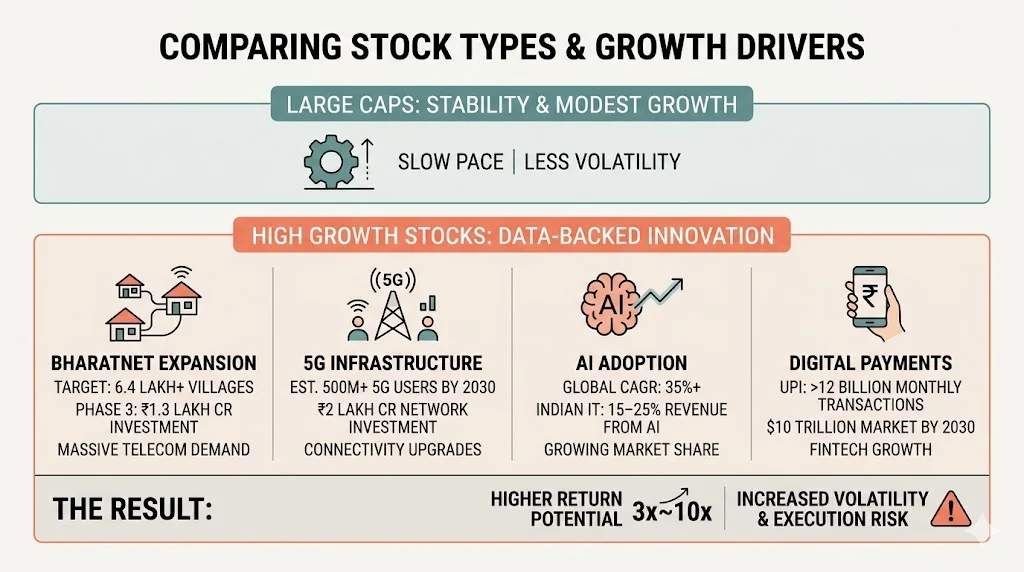

What Makes These Stocks Different From Large Caps

Large cap stocks provide stability. But they grow at a slower pace. High growth stocks are linked to new opportunities backed by strong data and measurable trends:

- BharatNet expansion: Over 6.4 lakh villages are targeted for fiber connectivity, with Phase 3 alone involving investments of ₹1.3 lakh crore, creating massive demand for telecom infrastructure companies

- 5G infrastructure: India is expected to have over 500 million 5G users by 2030, with telecom operators investing more than ₹2 lakh crore in network rollout and upgrades

- AI adoption: The global AI market is projected to grow at a CAGR of 35%+, and Indian IT companies are already seeing 15–25% revenue contribution from AI-driven services

- Digital payments growth: UPI transactions have crossed 12 billion per month, and the digital payments market in India is expected to reach $10 trillion annually by 2030

These strong growth drivers can lead to significantly higher return potential, often 3x to 10x in the long term. However, such opportunities also come with increased volatility and execution risk, making careful stock selection essential.

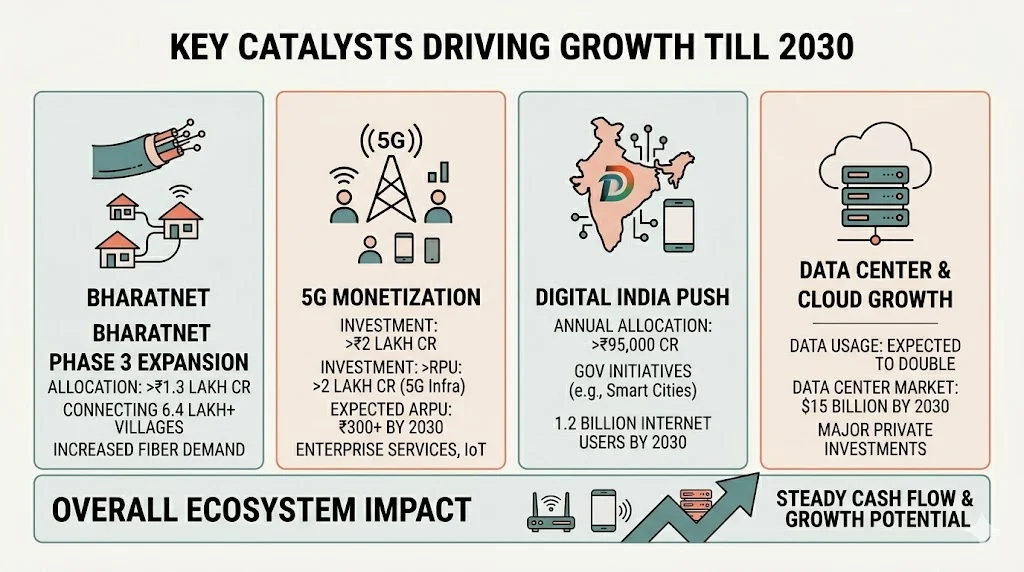

Key Catalysts Driving Growth Till 2030

BharatNet Phase 3 Expansion

BharatNet Phase 3 is one of the biggest growth drivers for telecom infrastructure companies. The government has allocated more than ₹1.3 lakh crore for this phase, aiming to connect over 6.4 lakh villages with high-speed fiber internet.

This massive rollout will significantly increase demand for optical fiber cables, routers, and network equipment. Companies like HFCL and Tejas Networks are direct beneficiaries, as they have already secured large contracts under this project. For example, HFCL’s order book has crossed ₹7,000 crore, while Tejas Networks has seen strong revenue visibility due to multi-year government contracts. This ensures steady cash flow and long-term growth potential.

5G Monetization

Till now, telecom companies have focused heavily on 5G rollout, investing more than ₹2 lakh crore collectively in spectrum and infrastructure. However, the next phase is monetization. Average Revenue Per User (ARPU) is expected to rise from the current ₹200–₹220 range to ₹300+ by 2030. This increase will come from premium 5G plans, enterprise services, IoT solutions, and private networks.

Companies like Bharti Airtel and Reliance Jio are already expanding into enterprise 5G services, which offer higher margins compared to retail users. This shift from capex-heavy rollout to revenue generation will improve profitability across the sector.

Digital India Push

The Indian government continues to invest aggressively in digital infrastructure, with annual allocations exceeding ₹95,000 crore. Initiatives like Digital India, Smart Cities, and e-Governance are driving demand for connectivity, cloud services, and cybersecurity solutions. Internet penetration in India has already crossed 900 million users and is expected to reach 1.2 billion by 2030.

This rapid digital adoption creates a strong demand base for telecom and IT companies. Additionally, government-backed projects provide long-term revenue visibility and reduce business uncertainty for companies involved in infrastructure development.

Data Center And Cloud Growth

India’s data consumption is growing at a rapid pace, with average monthly data usage already exceeding 30GB per user. This is expected to double by 2030 due to video streaming, gaming, and AI applications. As a result, the data center market in India is projected to grow from around $6 billion in 2024 to over $15 billion by 2030.

Major players like Reliance, Adani, and global cloud providers are investing heavily in building data centers across the country. Telecom and IT companies are benefiting from this trend through increased demand for fiber connectivity, cloud services, and network infrastructure. This creates a strong long-term growth opportunity for the entire ecosystem.

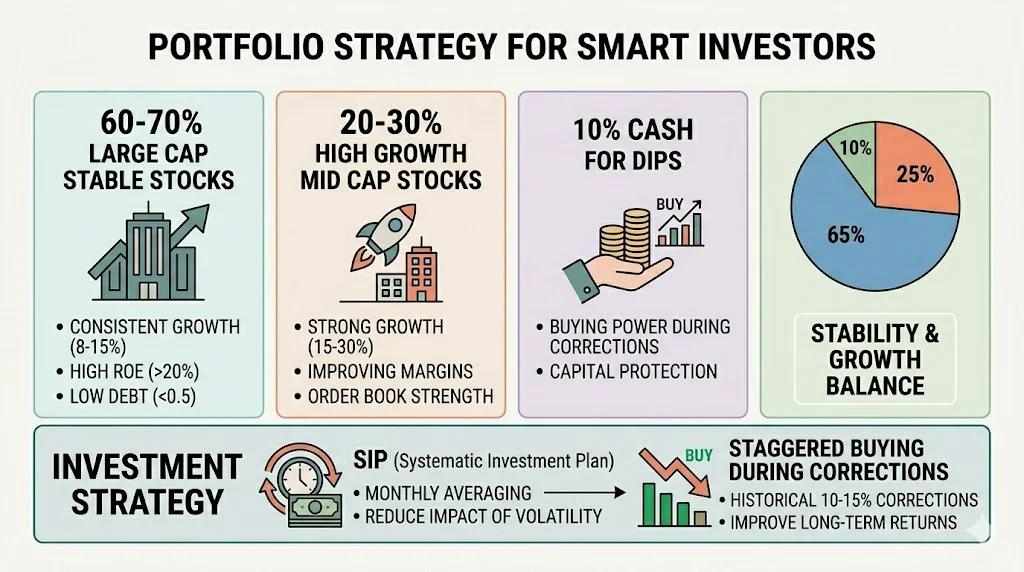

Portfolio Strategy For Smart Investors

You should not invest only in high risk stocks. A balanced approach works better because it helps you manage volatility and protect capital while still capturing growth.

Suggested Allocation

- 60 to 70 percent in large cap stable stocks (companies with consistent revenue growth of 8–15 percent, ROE above 20 percent, and low debt-to-equity below 0.5)

- 20 to 30 percent in high growth mid caps (companies growing revenue at 15–30 percent with improving margins and strong order books)

- 10 percent cash for buying during dips (to take advantage of 10–20 percent market corrections)

Investment Strategy

Use SIP method. Invest slowly over time. For example, instead of investing ₹1,00,000 at once, invest ₹8,000 to ₹10,000 monthly to average your buying price.

Buy during market corrections. Historically, markets correct 10–15 percent once or twice a year, which provides good entry points. Do not invest all money at once. Keep staggered entries to reduce risk and improve long term returns.

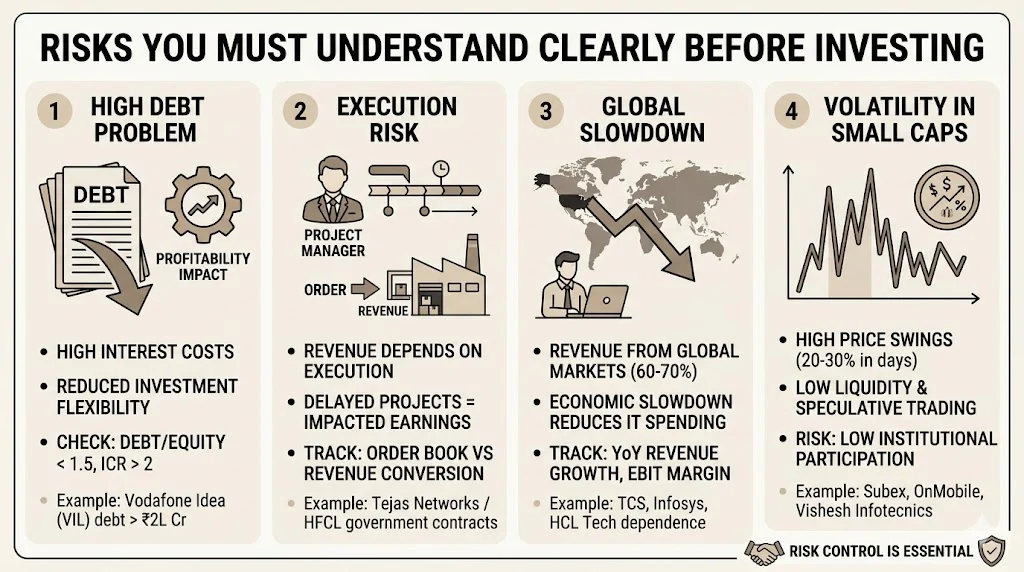

Risks You Must Understand Clearly Before Investing

1. High Debt Problem

Some telecom companies have very high debt levels, which directly impacts profitability and future growth. For example, Vodafone Idea has total debt of more than ₹2 lakh crore, including AGR dues and spectrum liabilities. Because of this, a large portion of its revenue goes into interest payments instead of expansion. Its interest cost alone is in thousands of crores annually, which keeps net profit negative.

Even Bharti Airtel, though financially stronger, carries debt of around ₹1.5 lakh crore. However, its higher ARPU (Average Revenue Per User) of ₹200+ helps it manage debt better compared to Vodafone Idea, whose ARPU is still around ₹150–₹160.

High debt reduces flexibility. Companies cannot invest aggressively in 5G, network expansion, or new services. Investors should always check:

- Debt to Equity ratio (ideal below 1.5 for telecom)

- Interest Coverage Ratio (should be above 2)

- Free Cash Flow trends

If these metrics are weak, growth can slow down significantly.

2. Execution Risk

Companies like Tejas Networks and HFCL depend heavily on project execution, especially government contracts like BharatNet Phase 3. For example, Tejas has received large orders worth ₹7,000+ crore, and HFCL has also secured significant contracts in fiber and router deployment.

However, revenue recognition depends on timely execution. If projects are delayed by even 6–12 months, it can impact quarterly earnings and stock price. For instance:

- Order book vs revenue conversion ratio becomes critical

- Execution delays can reduce margins due to cost overruns

- Working capital requirements increase

Investors should track:

- Order book size (Tejas has multi-thousand crore order book)

- Quarterly revenue growth consistency

- Operating margin trends (ideally above 15% for strong execution)

Strong order book is good, but execution speed decides actual returns.

3. Global Slowdown

IT companies like TCS, Infosys, and HCL Tech depend heavily on global markets, especially the US and Europe. Around 60–70% of their revenue comes from these regions. If global economies slow down, companies reduce IT spending.

For example:

- In slowdown periods, IT growth can drop from 12–15% to 5–7%

- Deal wins may remain strong, but execution gets delayed

- Attrition reduces, but pricing pressure increases

Key metrics to track:

- Revenue growth (YoY)

- Deal pipeline (large deal wins in $ terms)

- EBIT margin (usually 20–25% for top IT firms)

If US recession risk increases, IT stocks may underperform in the short term, even if long-term growth remains intact.

4. Volatility In Small Caps

Small cap and penny stocks like Subex, OnMobile, and Vishesh Infotecnics are highly volatile. These stocks can move 20–30% in a few days due to low liquidity and speculative trading.

For example:

- Subex has seen price swings from ₹5 to ₹40 and back in past cycles

- Penny stocks below ₹10 can double quickly but also fall 50% easily

- Daily trading volume is low, which increases price manipulation risk

Key risks include:

- Low promoter holding or frequent pledging

- Weak earnings visibility (inconsistent profits)

- Low institutional participation

Investors should:

- Limit allocation to 5–10% of portfolio

- Avoid chasing sudden rallies

- Focus on companies with improving revenue and profit trends

High volatility can create opportunities, but without strong fundamentals, downside risk is equally high.

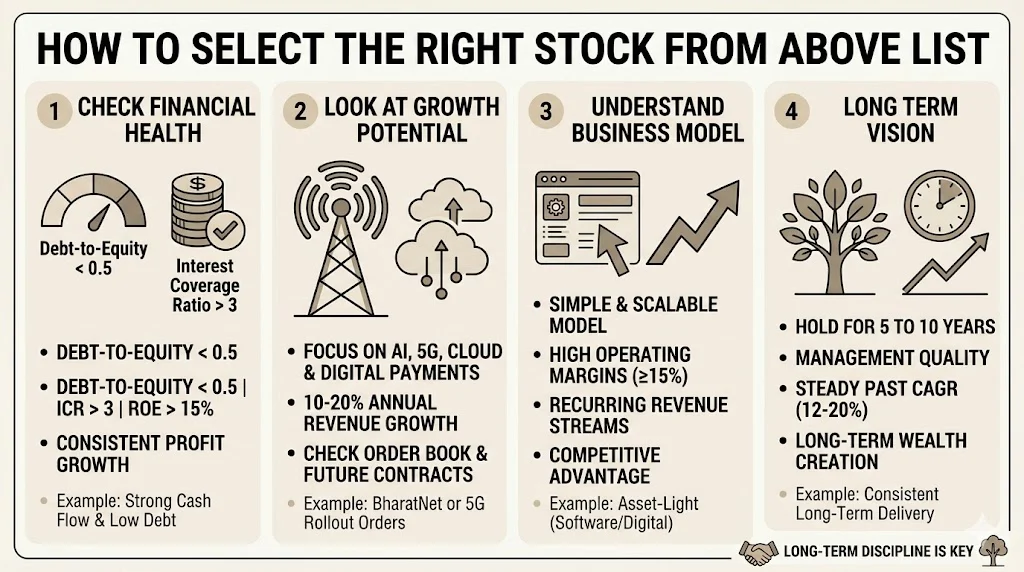

How To Select The Right Stock From Above List

1. Check Financial Health

Before investing, always look at key financial ratios. A Debt-to-Equity ratio below 0.5 is considered healthy for most companies. Interest Coverage Ratio should ideally be above 3, which shows the company can easily pay its interest. Also check Return on Equity (ROE) above 15% and consistent profit growth over the last 3 to 5 years. Companies with strong cash flow and low debt are more stable during market downturns.

2. Look At Growth Potential

Focus on industries with strong future demand like AI, 5G, cloud computing, and digital payments. Check revenue growth rate of at least 10% to 20% annually. Also look at order book size and future contracts. For example, companies involved in BharatNet or 5G rollout often have large confirmed orders, which ensures future revenue visibility.

3. Understand Business Model

A simple and scalable business model is always better. Look for companies with high operating margins (15% or more) and recurring revenue streams. Asset-light models, like software or digital services, usually scale faster compared to heavy infrastructure businesses. Also check if the company has a competitive advantage or unique product offering.

4. Long Term Vision

Invest only if you can hold for 5 to 10 years. Look at past performance consistency, management quality, and future expansion plans. Companies that have delivered steady CAGR of 12% to 20% over long periods are generally reliable. Avoid short-term speculation and focus on long-term wealth creation.

Frequently Asked Questions

What is Vodafone Idea share price target for 2030

Vodafone Idea target is estimated between ₹40 to ₹90 in optimistic scenarios. This depends on company survival and growth. From a fundamentals perspective, the company is currently operating with a high debt burden of over ₹2 lakh crore, which remains the biggest risk.

However, recent tariff hikes have helped improve ARPU (Average Revenue Per User) from around ₹135 to ₹150+, and further increases can support revenue growth. The company’s subscriber base is still above 200 million, which gives it a strong market presence if retention improves.

Government support through equity conversion and relief measures has also reduced immediate financial pressure. For the stock to reach higher targets, Vodafone Idea needs consistent ARPU growth above ₹200, successful 5G rollout, and reduction in losses over the next few years.

Is Tejas Networks a multibagger by 2030

Tejas Networks has strong potential due to BharatNet Phase 3 orders, where it has secured contracts worth over ₹7,000+ crore for supplying routers and optical networking equipment. The company’s order book has expanded significantly, providing strong revenue visibility for the next 2–3 years.

Financially, Tejas has shown improving fundamentals with revenue growth crossing ₹4,000 crore annually and a shift towards profitability after years of losses. Its EBITDA margins are expected to improve as large-scale deployments begin.

The company also benefits from strong backing by the Tata Group, which adds credibility and execution strength. If Tejas successfully executes these large government projects and continues to win 4G/5G equipment deals, it can become a multibagger by 2030, although investors should monitor execution timelines and margin expansion closely.

HFCL vs Tejas which is better?

Both are strong, but their fundamentals show clear differences. HFCL reported FY25 revenue of around ₹4,500–₹4,800 crore with EBITDA margins near 14–16% and a relatively manageable debt-to-equity ratio below 0.5, making it financially more stable. Its order book is estimated above ₹7,000 crore, driven by BharatNet and fiber projects, which provides good revenue visibility.

Tejas Networks, on the other hand, has seen sharp growth with FY25 revenue crossing ₹8,000 crore after large government and BSNL orders, but margins are more volatile due to execution-heavy projects. The company has a strong order book exceeding ₹10,000 crore, and its return ratios are improving, but earnings consistency is still evolving.

In simple terms, HFCL offers steadier financials and predictable growth, while Tejas Networks has higher upside potential due to large-scale contracts but comes with higher execution and earnings volatility risk.

My Final Thoughts On Best Tech & Telecom Stocks

If you only stick to popular stocks, you might feel safe, but you could also miss out on some of the biggest opportunities. In my experience, real wealth is often built by spotting future leaders early and giving them time to grow.

The tech and telecom sectors are not just another trend. They are slowly becoming the backbone of India’s future. That is why this space deserves your attention. At the same time, it is important to stay grounded. High returns always come with higher risk. So instead of chasing quick gains, focus on building a balanced portfolio that you can hold with confidence.

Personally, I believe a simple approach works best. Keep strong large cap stocks for stability. Add a few high growth bets for upside. Invest regularly, even in small amounts, and most importantly, stay patient. If you can follow this with discipline and avoid emotional decisions, the next 5 to 10 years can truly change your financial journey.

Related Posts :

Share This Post